Plotting code for the essay is in a Jupyter notebook.

Introduction

What this essay contains

This essay works through what is typically contained in a university course on analytical mechanics. The prerequisites are multivariate calculus and mathematical maturity.

It covers: calculus of variations, Lagrangian, Legendre transform, Hamiltonian, Hamilton’s principal function, Hamilton–Jacobi equation, the particle-wave duality, contact geometry, symplectic geometry, Poisson bracket, canonical transformations, infinitesimal generator, Schrödinger’s equation, Hamilton’s geometric optics, action-angle variables, general relativity, Noether’s theorem, adiabaticity, old quantum theory, Bohr–Sommerfeld quantization, Einstein–Brillouin–Keller quantization.

It does not cover: virtual work, d’Alembert’s principle, canonical perturbation theory, continuum mechanics, rigid bodies, field theory.

Philosophically, this essay has two undercurrents:

One, that thinking on the margins is vital not just in economics, but also in classical mechanics. In my other essay, Classical thermodynamics and economics, I show that classical thermodynamics is also nothing more than thinking on the margins.

Two, classical mechanics is a leakless leaky abstraction. Though classical mechanics has many equivalent forms, the search for the most elegant form has led us to the Hamilton–Jacobi equation, and the adiabatic theorem, both of which were on the threshold of quantum mechanics. Even though classical mechanics is a self-consistent closed world (thus “leakless”), when viewed in the right light, all its lines and planes seem to angle towards a truer world (thus “leaky”), of which this world is merely a shadow (thus “abstraction”).

Conventions

We always assume all functions are analytic (that is, they have Taylor expansions).

We would often say “minimize cost” or “maximize revenue” or such, but we always mean “stationarize”. For example, when we say “Let’s maximize f(x)”, what we mean is “Let’s solve f'(x) = 0”. If we were to actually maximize f(x), we would have to check f''(x) < 0 as well, but we don’t. This is not a problem for physics, where the principle of stationary action rules. However, in optimal control and economics, we should check if the solution is actually a minimum/maximum.1

1 Thus, the analogy between classical mechanics and economics is not precise. However, the analogy is precise between classical thermodynamics and economics, since the entropy is actually maximized, and not merely stationarized.

Instead of laboriously typing \vec q or \mathbf{q}, I just write q = (q_1, \dots, q_n), unless there is a serious risk of confusion.

| Symbol | Mechanics | Economics | Control Theory |

|---|---|---|---|

| L | Lagrangian | time-rate of cost | time-rate of cost |

| t | time | time | time |

| q | location/coordinate | commodity | state variable |

| \dot q | velocity | production rate/consumption rate | control variable |

| S = \int L(t, q, \dot q)dt | action | total cost | total cost |

| p | momentum | price | co-state variable |

| H = \sum_i p_i\dot q_i - L | Hamiltonian | market equivalent cash flow2 | Hamiltonian |

2 also known as “mark to market cash flow”

Why I wrote this

I wrote this as “Analytical Mechanics done right”, or “What every graduate student in physics should know about analytical mechanics, but didn’t learn well, because the textbooks are filled with too many symbols and not enough pictures.”, or “what I wish the textbooks to have said when I first learned the subject”.

In my physics Olympiad years, I saw the Lagrangian a few times, but we had no use for that. During my undergraduate years, I studied analytical mechanics. The construction of the Lagrangian was reasonable enough, and I understood how the Euler–Lagrange equation was derived by \delta \int L = 0. However, as soon as they proceeded to the Hamiltonian, I was entirely lost.

What is H(p, q) = p \dot q - L(q, \dot q)? Why does the right side depend on \dot q but not the left side? How does anyone just make up the Legendre transform out of thin air? It’s named “Legendre transform” – well, if it has such a fancy name, surely this has many more applications than H = p \dot q - L, else, why not call it “Legendre’s one-time trick”? Canonical transform? Point transform? Aren’t they all coordinate transforms? Poisson bracket? Infinitesimal generators? It was all a giant mess. Reading Goldstein’s classic textbook only made my confusion more well-rounded.

Early 2023, I studied mathematical microeconomics. When I was studying Ramsey’s theory of optimal saving, I saw, to my great surprise, something they call a “Hamiltonian” (Campante, Sturzenegger, and Velasco 2021, chap. 3). I was shocked, but after studying it carefully, and thinking it over, I realized that it was no mistake – the “Hamiltonian” in economics and in physics really are the same. Physics has an economic interpretation. Everything fell into place over the course of a few hours. Guided by this vision, I worked through analytical mechanics again, this time with true understanding.

It is my experience that everything in undergraduate physics is taught badly, except perhaps Newtonian mechanics. I have written this essay to make analytical mechanics finally make sense. It has made sense for me, and I hope it will make sense for you.

Optimization as making money

The shortest line problem

In this problem, the so-called “time” t has units of length as well. So, please don’t panic when we see something like \sqrt{1 + \dot x^2}. If it worries us, we can replace t by v\tau, where v is a constant speed of one, and \tau is time.

Start with the easiest problem: shortest path problem. What is the shortest path from (0, 0) to (A, B)? We parametrize the path by a function t \mapsto (x(t), y(t)), with t\in [0, 1]. The problem is then

\begin{cases} \min \int_0^1 \sqrt{\dot x^2 + \dot y^2}dt \\ \int_0^1 \dot x dt = A \\ \int_0^1 \dot y dt = B \\ \end{cases}

This is a standard constraint-optimization problem, and could be solved by the Lagrangian multiplier method:

\delta \left(\int_0^1 \sqrt{\dot x^2 + \dot y^2}dt + p_x \left( A - \int_0^1 \dot x dt\right) + p_y \left( B - \int_0^1 \dot y dt\right) \right) = 0

where p_x, p_y are the Lagrangian multipliers, each responsible for enforcing one constraint.

Varying the path functions x, y gives us

\delta \int_0^1 (\sqrt{\dot x^2 + \dot y^2} - p_x \dot x - p_y \dot y)dt = 0

Each of \dot x, \dot y could be independently perturbed with a tiny concentrated “pulse”, so for the integral to be stationary, the integrand must be zero with respect to derivatives of \dot x, \dot y. That is, we have

\begin{cases} \partial_{\dot x}(\sqrt{\dot x^2 + \dot y^2} - p_x \dot x - p_y \dot y )= 0\\ \partial_{\dot y}(\sqrt{\dot x^2 + \dot y^2} - p_x \dot x - p_y \dot y ) = 0 \end{cases}

and we are faced with the solution

(p_x, p_y) = \frac{1}{\sqrt{\dot x^2 + \dot y^2}}(\dot x, \dot y)

Since p_x, p_y are independent of time, they are constants, and since we have from the above equation p_x^2 + p_y^2 = 1, we find that p_x = \cos\theta, p_y = \sin\theta for some \theta. Thus, the curve is a straight line making an angle \theta to the x-axis.

Economic interpretation

Interpret x, y as two goods that we can produce (let’s say, tons of steel and tons of copper).

We are a factory manager, and we are given a task: produce A of x (tons of steel), and B of y (tons of copper), in [0, 1] (one year). If we don’t do it, we will be sacked. Our problem is to accomplish the task at minimal cost.

\dot x, \dot y are the speed at which we produce the goods, which we can freely control. In control theory, we say x, y are state variables, and \dot x, \dot y are control variables.

The cost function is L(t, x, y, \dot x, \dot y) = \sqrt{\dot x^2 + \dot y^2}. Its integral S = \int_0^1 L dt is the total cost of production, which we must minimize.

We are also given a free market on which we are allowed to buy and sell the goods. If we cannot achieve the production target, we buy from the market. If we achieve more than the production target, we sell them off.

Then, the total cost is

\left(\int_0^1 \sqrt{\dot x^2 + \dot y^2}dt + p_x \left( A - \int_0^1 \dot x dt\right) + p_y \left( B - \int_0^1 \dot y dt\right) \right)

where p_x, p_y are the market prices which do not change with time.

If our production plan is optimal, then the plan must have stationary cost. That is, if we make a change in our production plan (\dot x, \dot y) by O(\delta), our production cost must not change by O(\delta), or else we could achieve lower cost. For example, if the plan (\dot x + \delta \dot x, \dot y + \delta \dot y) achieves higher cost, then (\dot x - \delta \dot x, \dot y - \delta \dot y) achieves lower cost.

Mathematically, it means the optimal production plan must satisfy

\delta \left(\int_0^1 \sqrt{\dot x^2 + \dot y^2}dt + p_x \left( A - \int_0^1 \dot x dt\right) + p_y \left( B - \int_0^1 \dot y dt\right) \right) = 0

Now, the great thing about the market is that it is always there and we can trade with it, So, we have completely transformed the question into a problem of profit maximization – we’ll always sell to the market, and then buy back from the market right at the end.

Now we can perform profit maximization moment-by-moment: raise production until marginal profit reaches cost:

\begin{cases} \partial_{\dot x}(\sqrt{\dot x^2 + \dot y^2} - p_x \dot x - p_y \dot y )= 0\\ \partial_{\dot y}(\sqrt{\dot x^2 + \dot y^2} - p_x \dot x - p_y \dot y ) = 0 \end{cases}

which may be solved as before.

Now we can interpret p_x, p_y. What are they? Suppose we perturb \dot x by \delta \dot x, then since the production plan is already optimal, we have

\delta \left(\int_0^1 \sqrt{\dot x^2 + \dot y^2}dt + p_x \left( A - \int_0^1 \dot x dt\right) + p_y \left( B - \int_0^1 \dot y dt\right) \right) = 0

that is,

p_x \delta \int_0^1 \dot xd t = \delta\int_0^1 \sqrt{\dot x^2 + \dot y^2}dt

We have our interpretation p_x: the marginal cost of producing one unit of steel, That is, if we want an extra \delta A, we have to incur an extra cost p_x \delta A. It can thus be called the neutral price of steel. If the price were lower, we would rather buy steel from the market than produce steel ourselves, and vice versa. At the neutral price, we could use the market, but we have no reason to, since we can’t profit from doing so.

We actually have p_x = \cos \theta, p_y = \sin\theta, which means that when x, y are perturbed by \delta x, \delta y, the shortest length between them is perturbed by

p_x \delta x + p_y \delta y = \cos\theta \delta x + \sin\theta \delta y

which is clearly true by geometry.

We actually don’t need an external market. We could have put up such a fictional market inside the factory, and simply read out its price p_x, p_y without ever trading with it. Why? Because in this problem, a solution exists, and under some niceness assumptions, there exists a “fair” market price at which we are indifferent to trading with the market – we can sell \delta x and buy \delta y, but there is “no point to it” because it doesn’t change our eventual cost. Thus, although the market exists, we never actually trade with it, so the market might as well be a card-board cutout with a number display of the latest prices. As long as we don’t actually try to trade with it, we would be behaving exactly as if we are facing a real market with the same prices.

It is perhaps best to think of the markets as things inside the head, a system of mental accounting to assign the proper price of everything. If the market prices are truly efficient, then we don’t need a real market to trade with.

When the producer is ready, the market appears.

When the producer is truly ready, the market disappears.

Lagrange’s devil at Disneyland

This is a parable about maximizing entropy under conservation of energy.

You are going to an amusement park, with many amusements i = 1, 2, \dots, n. You have exactly 1 day to spend there, so you need to spend p_i of a day on amusement i. Now, your total utility at the end of the day is

S(p) := \sum_i p_i \ln \frac{1}{p_i}

a sum of logarithms, the idea being that you gain utility on any amusement at a decreasing rate: The first minute on the rollercoaster is great, but the second is less, and the third even less.

If that’s all there is to the amusement park, then the solution is clear: you should spend an equal amount of time at each amusement. This can be proved by the Lagrange multiplier mechanically, but underneath the algorithm of the Lagrange multiplier is the idea of partial equilibrium, so it’s worth spelling it out in full.

Suppose your parents give you a schedule for your amusement. You look at the schedule and notice that p_i < p_j. You can reject the plan and say, “I can always do better just by spending equal time at i, j, even holding the other times fixed.”. That is, if we are only allowed to trade between time at i and j (a “partial market”), then at partial market equilibrium, the marginal utility of amusements i, j must be equal.

The marginal utility of amusement i is \ln(1/p_i) - 1, and the same for j. So, at partial equilibrium, p_i = p_j, and at general equilibrium, all partial markets are in partial equilibrium.

Unfortunately, the amusement park is actually infinite. You can take this news in two ways: optimistically “I can earn arbitrarily high utility by spending 1/N of a day on N amusements each, and let N be as large as I want!” and pessimistically “No matter how much I try, I can never achieve the perfect day.”. Fortunately, the amusement park has a token system: when you enter the park, you would buy a certain number of tokens. Then you spend some tokens at the rides, proportional to the time you spend there.

There are some rules to the game:

- You will be given a certain number of tokens E at the start of the day.

- The prices of amusements are 0 = E_0 \leq E_1 \leq E_2 \leq \cdots. Here E_0 is the “zero-point energy”, or in other words, “just relax”.

- You must spend exactly all your tokens. Your parents hate wastefulness and would beat you up if you don’t use all the tokens.

- Your parents are kind enough to supply you with the right number of tokens E, such that you can avoid getting beat up: E_0 \leq E \leq \max_i E_i.

Thus we have reduced the problem to \begin{cases} \max S(p) \\ \sum_i p_i \cdot 1 = 1 \\ \sum_i p_i \cdot E_i = E \end{cases}

Under these assumptions, there exists a unique schedule that maximizes your fun, or entropy.

Now there is a slight difficulty with your previous approach. Doing partial equilibrium between 2 amusements is not possible now, because you have two constraints of not just time, but also tokens. Suppose you spend less time at i to spend more time at j, this might cause you to under- or over-spend your tokens. So, to make a partial equilibrium calculation, you must use at least 3 amusements, not 2. And you are not allowed to “just relax”, since relaxing is actually “the 0th amusement”, and thus it also costs you tokens and time. That is, you must open partial markets with i, j, k at once, and then you can run the system to partial equilibrium. This is pretty annoying. There’s got to be a better way.

Suddenly, in a puff of smoke, Lagrange’s devil makes an appearance!

- “You can’t solve the general equilibrium problem, you say? Why not try the Lagrange multipliers?”

- “Too annoying.”

- “Alright, how about I make you a deal –”

- “Sorry, but I don’t sell my soul.”

- “Don’t be stupid – only something as stupid as God could still believe in souls these days! I am proposing that you trade happiness for time and for tokens. I will make a set price for time and another set price for tokens. Both prices are in units of your happiness. You can buy happiness with time, or time with happiness, also for tokens.”

- “Uhmm…”

- “That’s all that I offer. You should read up on microeconomics so you can make the right choice. See you when the day comes!”

So the day comes and the devil shows up with the two prices:

- 1 unit of time = \alpha unit of utility.

- 1 unit of token = \beta unit of utility.

So you solve the following problem

\max_p \left(S(p) - \alpha \sum_i p_i - \beta \sum_i p_i E_i\right)

What a great luck that the devil is there – it has split a giant, intercorrelated general equilibrium into so many little, uncorrelated partial equilibria: \forall i,\quad \max_{p_i} \left(p_i \ln \frac{1}{p_i} - \alpha p_i - \beta p_i E_i\right)

with solution p_i = e^{-1-\alpha} e^{-\beta E_i}.

You are about to go to the devil, but then the devil waves at you to halt, “Don’t make individual trades, but make a bulk one-time trade.”. So you calculate \sum_i p_i and \sum_i p_i E_i, and to your surprise, you find that they equal exactly 1 and E. That is, you actually would spend all your time and tokens without needing to trade with the devil.

And so you sits there, looking at your two equations in strange amusement:

p_i = \frac{e^{-\beta E_i}}{e^{1+\alpha}}, \quad \alpha+1 = \ln\sum_i e^{-\beta E_i} , \quad E = \sum_i E_i \frac{e^{-\beta E_i}}{e^{1+\alpha}}

A physicist comes and points out that they are better known as

p_i = \frac{e^{-\beta E_i}}{Z}, \quad Z = e^{-\beta F} = \sum_i e^{-\beta E_i}, \quad E = \sum_i p_i E_i

where Z is called “partition function”, F “Helmholtz free energy”, and \beta “inverse temperature”.

As the devil prepares to leave, you call after it:

- “I’m grateful for all your help, but, please why did you price your wares this way?”

- “Because I don’t want you to actually be happier!”

- “What do you mean?”

- “If I were to lower the price of tokens, then what would you do? You would realize that you can profit by spending a little less time at every amusement, then sell both the time and the tokens you saved, increasing your happiness! Similarly for any other form of price change. If I priced it in any other way than the equilibrium prices, you would be able to exploit my bad pricing and arbitrage out some happiness.”

- “So why did you come to visit me in the first place?”

- “It was easy to mess with mortals back before you discovered calculus. Now all I do is help you people discover general equilibrium, because you people have no fun anymore – every arbitrage opportunity is exploited to death. Still, I have to come, because I am the CEO of Hell, and I need to make maximally profitable deals with mortals, no matter how pointless it is.”

When the mortal is ready to make a deal, the devil appears.

When the mortal is truly ready to make a deal, the devil disappears.

Isoperimetric problem

If we have a rope of length S, and wish to span it from (0, 0) to (T, h), what shape should the rope have, in order to maximize the area under the rope? In formulas, we model the rope as a differentiable function x(t): [0, T] \to \mathbb R, such that

\begin{cases} \max \int_0^T xdt\\ \int_0^T \sqrt{1 + \dot x^2}dt = S \\ \int_0^T \dot x dt = h \end{cases}

Here we have two constraints, but the solution is essentially the same. First, to take care of the two constraints, we open two markets p_h, p_S – one for the price of height, and another for the price of rope. Then, solve for

\delta \int_0^T \left(x + p_h \left(\frac hT - \dot x\right) + p_S\left(\frac ST - \sqrt{1+\dot x^2}\right)\right) dt = 0

The state variable is x, and the control variable is \dot x. Unlike the previous problem, here we need to maximize the integral of the state variable. Consequently, we consider it as a problem of “profit flows”.

To make things more clear, let’s explicitly write v as a control variable, and say that the control system satisfies:

\begin{cases} v \text{ is a control variable}\\ x \text{ is a state variable}\\ \dot x = v \end{cases}

Given that, how do we control the system? Again, it comes down to putting a price on everything, and greedily maximizing profit at every instant. So, let’s open one more market, this time on commodity x, such that the “fair” price is p(t) at time t. We can interpret this as follows: x is the number of area-producing machines, and v is the rate at which we are producing the area-producing machines. We are tasked with producing exactly h number of area-producing machines during the time period of [0, T]. The supervisor does not care what we are going to do with the area-producing machines. So, our plan is to first over-produce the machines and use these machines to produce area, which we can sell to the market and pocket the profit, then destroy some of the machines that we wouldn’t need anymore.

With that interpretation, we can write down the moment-by-moment profit flow:

H = x + p_h \left(\frac hT - v\right) + p_S\left(\frac ST - \sqrt{1+v^2}\right) + p v

Then, maximizing profit over all time implies maximizing profit flow at every instant:

\partial_v H= 0

This gives us one equation, but we need one more equation. Namely, we need to know how p(t), the “fair” price of the machinery x, changes with time. Unlike the price of area and height, which are constants that we work with, the price of machinery quite reasonably could change over time. At the beginning of time, machines are valuable, because there is still much time to produce area with. Near the end of time, machines become worthless to us, because we don’t have the time to produce more area. Thus, intuitively, the value of a machine should decrease with time linearly. Can we justify this more rigorously?

The fundamental problem in pricing theory is this: how do we put a price on something? The fundamental reply from pricing theory is: no-arbitrage (no free money).

Here is how the no-arbitrage argument works. Suppose that we have been following our optimal production plan. Then at time t, we suddenly decide to buy an extra \delta x from the market, save it, then sell \delta x at time t+ \delta t.

Now, since \dot x = v, this buying-and-selling plan does not change how much x grows, so after time \delta t, we have \delta x(t + \delta t) = \delta x(t). Thus, the no-arbitrage equation states:

p(t)\delta x(t) = p(t + \delta t)\delta x(t + \delta t) + \delta x(t) \delta t \implies p(t+ \delta t) = p(t) - \delta t

and consequently, \dot p = -1. This is the price dynamics, matching our intuition. Intuitively, we see that the value of a machine decreases linearly as we run out of time to use it for producing area.

To solve

\partial_v H= 0

first expand it to

-p_h + p - p_S \frac{\dot x}{\sqrt{1 + \dot x^2}} = 0

then take derivative with respect to t, to obtain

-\frac{\ddot x}{(1+\dot x^2)^{3/2}} = \frac{1}{p_S}

From elementary calculus, we know the item on the left is the curvature, so we find that the line x(t) is a constant-curvature curve – circular arc. The radius of the circle is the inverse of curvature, which is exactly p_S. Thus we find that, if we are given \delta S more rope, we can encircle R\delta S more area under the rope, where R is the radius of curvature for the circular arc.

Notice that there we are not given the sign of p_S. There are in general two solutions, one being a circular arc curving downwards, and the other curving upwards. If we use p_S < 0, then we get the one curving upwards, and so we get the solution that achieves minimal area under the rope. If we use p_S > 0, then we get the maximal solution. This is a general fact about such problems.

Lagrangian and Hamiltonian mechanics

Generalizing from our experience above, we consider a generic function L(t, q, v), with finitely many state variables q_1, ..., q_N. For each state variable q_i, we regard its time-derivative as a control variable v_i, which we are free to vary. Our goal is to design a production plan t \mapsto v(t), such that

\delta \int L(t, q(t), v(t)) dt = 0, \quad \dot q = v

To comply with general sign conventions, we interpret L as cost-per-time, so we say we want to minimize it (even though we only want to stationarize it).

We can understand i\in\{1, 2,..., N\} to denote a commodity, say timber and sugar (let’s say there is such a thing as “negative 1 ton timber” – that is, we can short-sell commodities). Let p_i be the market price of commodity i. Again, there is no need for real market to trade with if the prices are right, since at the right price (no-arbitrage price), we are indifferent between buying and selling, or producing and consuming. It is purely a “mental accounting” device.

With access to a market, our profit flow is:

H(t, q, p, v) := \underbrace{\sum_i p_i v_i}_{\text{revenue flow}} - \underbrace{L(t, q, v)}_{\text{cost flow}}

In words, H(t, q, p, v) is the rate of profit at time t if we hold a stock of commodity q, is producing at rate v, and the market price of commodities is p. This is close to the Hamiltonian, but not yet. We still need to remove the dependence on v.

Moment-by-moment profit-flow maximization is myopic, and could lead us into deadends. That is, it is not a sufficient condition for global profit-maximization. However, it is a necessary condition. That is, suppose we are given a profit-maximizing trajectory, then it must maximize profit flow at every moment, since otherwise we could improve it. In formula:

v = \mathop{\mathrm{arg\,max}}_v \left(\sum_i p_i v_i - L(t, q, v)\right)

So, define the “optimal controller” as

v^\ast (t, q, p) = \mathop{\mathrm{arg\,max}}_v \left(\sum_i p_i v_i - L(t, q, v)\right)

and define H as the “maximal profit flow” function:

H(t, q, p) = \max_{v} \left(\sum_i p_i v_i - L(t, q, v)\right) = \sum_i p_i v_i^\ast(t, q, p) - L(t, q, v^\ast(t, q, p))

By basic convex analysis, if L is strictly convex with respect to v, then v^* is determined uniquely by (t, q, p), and furthermore, it is a continuous function of (t, q, p). Consequently, “profit maximization” allows us to model the system in (t, q, p) instead of (t, q, v) coordinates, and the dynamics of the system is equivalently specified by either H or L.

This is the mysterious “Legendre transform” that they whisper of. It is better called “convex dual”. I also like to joke that the real reason that momentum is written as p is because it secretly means “price”!

Derivatives of H

Theorem 1 (Hotelling’s lemma) H(t, q, p) is differentiable with respect to p, and \begin{cases} \partial_t H(t, q, p) &= -(\partial_t L)(t, q, v^\ast(t, q, p)) \\ \nabla_p H(t, q, p) &= v^\ast(t, q, p) \\ \nabla_q H(t, q, p) &= -(\nabla_q L)(t, q, v^\ast(t, q, p)) \\ \end{cases}

We prove the first formula. The other two are proved in the same way.

The argument is by no-arbitrage. We can imagine what happens if we were to suffer a little price-shock \delta p, adjust our production plan accordingly to v + \delta v, then hold that production plan and suffer another little price-shock -\delta p. Since we are back to the original price p again, we should have no more than the maximal profit rate. That is, we should have

\underbrace{H(t, q, p)}_{\text{maximal rate before shock}} \geq \underbrace{H(t, q, p+\delta p)}_{\text{maximal rate after shock}} + \underbrace{\langle -\delta p, v^\ast(t, q, p+\delta p) \rangle}_{\text{undoing the shock, holding price steady}}

Since \delta p is infinitesimal, this implies \left\langle-\delta p , \nabla_v H\right\rangle \geq \left\langle-\delta p , v^*(t, q, p)\right\rangle + O(\delta^2) for all \delta p, implying \nabla_v H = v^\ast(v^*(t, q, p)).

Here, we explicitly put a bracket around \partial_t L to emphasize that

\begin{aligned} (\partial_t L)(t, q, v^\ast(t, q, p)) &= \lim_{\epsilon \to 0} \frac{L(t + \epsilon, q, v^\ast(t, q, p)) - L(t, q, v^\ast(t, q, p))}{\epsilon} \\ &\neq \lim_{\epsilon \to 0} \frac{L(t + \epsilon, q, v^\ast(t + \epsilon, q, p)) - L(t, q, v^\ast(t, q, p))}{\epsilon} \end{aligned}

and similarly for \nabla_q L.

Hamiltonian equations of motion

We are given free control over \dot q, and we saw that the cost-minimizing trajectory must maximize the profit flow moment-by-moment. That is,

\dot q(t) = v^\ast(t, q(t), p(t)) = (\nabla_p H)(t, q(t), p(t))

or more succinctly (you can see why we tend to be rather sloppy with notations!)

\dot q \underbrace{=}_{\text{optimality}} v^\ast \underbrace{=}_{\text{Hotelling's lemma}} \nabla_p H

More evocatively speaking, we have two opposing forces of greed and no-arbitrage, clashing together to give something interesting:

\dot q \underbrace{=}_{\text{we are greedy}} v^\ast \underbrace{=}_{\text{but the market gives us no free money}} \nabla_p H

It remains to derive \dot p by the no-arbitrage condition: If we shock the system with some \delta q_i, it does not matter if we sell it now, or carry it \delta t, incurring additional cost, and sell it later. That is,

p_i(t) \delta q_i = p_i(t+\delta t) \delta q_i - \partial_{q_i} L(t, q, v) \delta q_i \delta t \implies \dot p_i = \partial_{q_i} L(t, q, v)

The equality should be more precisely read as “up to a higher-order infinitesimal than \delta q_i\delta t”. That is, we should be writing:

p_i(t) \delta q_i = p_i(t+\delta t) \delta q_i - \partial_{q_i} L(t, q, v) \delta q_i \delta t + o(\delta q_i\delta t)

This detail would come up later in our proof of the Hamilton–Jacobi equation.

Since we are only concerned with what happens on the optimal trajectory, we always choose v = v^\ast, so

\dot p_i = (\partial_{q_i} L)(t, q, v^\ast(t, q, p)) \underbrace{=}_{\text{Hotelling's lemma}} -\partial_{q_i} H(t, q, p)

Thus, we obtain the two fundamental equations of Hamiltonian mechanics:

Theorem 2 (Hamilton equations of motion) \begin{cases} \partial_t H &= -\partial_t L \\ \dot p &= -\nabla_q H \\ \dot q &= \nabla_p H \end{cases}

Euler–Lagrange equations of motion

By definition,

H(t, q, p) = \max_{v} \left(\sum_i p_i v_i - L(t, q, v)\right) = \sum_i p_i v_i^\ast(t, q, p) - L(t, q, v^\ast(t, q, p))

and since L is strictly convex in v, this can be inverted (this is called “convex duality”) to give

L(t, q, v) = \max_{p} \left(\sum_i p_i v_i - H(t, q, p)\right) = \sum_i p^\ast_i v_i - H(t, q, p^\ast(t, q, p))

where p^\ast = \mathop{\mathrm{arg\,max}}_p \sum_i p_i v_i - H(t, q, p). It is a basic theorem in convex geometry that, if L is strictly convex in v, then H is strictly convex in p, so the inversion works.

By the same argument as in Hotelling’s lemma, we have

\nabla_v L(t, q, v) = p^\ast(t, q, v)

By definition of the convex dual, for any t, q, p, v, we have

H(t, q, p) + L(t, q, v) \leq \sum_i p_i v_i

with equality reached iff both p = p^\ast(t, q, v) and v = v^\ast(t, q, p). Thus, on any optimal trajectory, since v = v^\ast(t, q, p), we must also have p = p^\ast(t, q, v), and consequently,

\frac{d}{dt} \nabla_v L \underbrace{=}_{\text{Hotelling's lemma}} \dot p^\ast \underbrace{=}_{\text{optimality}} \dot p \underbrace{=}_{\text{no-arbitrage}} \nabla_q L

This is the famous

Theorem 3 (Euler–Lagrange equations of motion) \frac{d}{dt} (\partial_{v_i} L) = (\partial_{q_i} L) \quad \forall i \in \{1, 2, \dots, N\}

or more succinctly,

\frac{d}{dt} (\nabla_v L) = \nabla_q L

Physicists are often sloppy with notations, but the Euler–Lagrange equation is particularly egregious in this regard, so I will describe it carefully.3

The function L is a function of type \underbrace{\mathbb{R}}_{\text{time}} \times \underbrace{\mathbb{R}^N}_{\text{state}} \times \underbrace{\mathbb{R}^N}_{\text{control}} \to \mathbb{R}.

The function \partial_{v_i} L is also a function of type \mathbb{R}\times \mathbb{R}^N \times \mathbb{R}^N \to \mathbb{R}. It is obtained by taking derivative of L over its (1 + i)-th input. Let’s write that as f_i to make sure we are not confused by it. It is absolutely important to be clear about this! f_i is not a function defined only along a trajectory, but over the entire space of \mathbb{R}\times \mathbb{R}^N \times \mathbb{R}^N. We can similarly define f_{i + N} to be \partial_{q_i} L.

Now, suppose we are given a purportedly optimal trajectory q: \mathbb{R}\to \mathbb{R}^N, then for any coordinate i \in \{1, 2, \dots, N\}, we can define a function g_i, of type \mathbb{R}\to \mathbb{R} by

g_i(t) = f_i(t, q(t), \dot q(t))

and similarly, we can define g_{i + N} = f_{i + N}(t, q(t), \dot q(t)).

The Euler–Lagrange equations say that we need only check

g_i'(t) = g_{i+N}(t) \quad \forall t \in [0, T], i \in 1:N

to certify that the purportedly stationary trajectory q is truly stationary.

3 I am okay with sloppy notation sometimes, but in this case, the sloppy notation often leads to calculational mistakes and conceptual confusions, as teachers of undergrad courses can testify.

In 1930, Herglotz proposed a generalization of Lagrangian mechanics, by making the Lagrangian L depend on the path-action-so-far S:

\begin{cases} \delta S(t_1) = 0\\ \dot S (t) = L(t, \gamma (t), \dot \gamma (t), S(t)), & t \in [t_0, t_1] \\ S(t_0) = S_0 \\ \gamma \text{ has end points } t_0, q_0, t_1, q_1 \end{cases}

This can be interpreted economically as saying that money itself has effect on our profit. For example, suppose that L = \frac 12 v^2 - S, then it says that the more cost we have incurred during the production, the less further production would cost. Perhaps this can be interpreted as saying that there is now a transaction subsidy/cost that depends on how much money we currently have. This interpretation suggests that we can model friction this way, and indeed Herglotz mechanics is often used to model systems with friction.

Most derivations in this essay still work as long as you account for the transaction subsidy/cost. So, as you read, you are welcome to rederive all the equations for Herglotz mechanics:

\begin{aligned} &\begin{cases} H(t, q, p, S) &= \max_v (\braket{p, v} - L(t, q, v, S)) \\ v^*(t, q, p, S) &= \mathop{\mathrm{argmax}}_v (\braket{p, v} - L(t, q, v, S)) \\ L(t, q, v, S) &= \min_p (\braket{p, v} - H(t, q, p, S)) \\ p^*(t, q, v, S) &= \mathop{\mathrm{argmin}}_p (\braket{p, v} - H(t, q, p, S)) \end{cases} \quad \text{(convex duality)} \\ &\begin{cases} (\partial_t, \nabla_q, \partial_S) H &= -(\partial_t, \nabla_q, \partial_S) L \\ \nabla_p H &= v^*\\ \nabla_v L &= p^* \end{cases} \quad \text{(Hotelling's lemma)} \\ &\begin{cases} \dot S &= \braket{p, \nabla_p H} - H \\ \dot p &= \nabla_p H \\ \dot q &= -(\nabla_p H + p \partial_S H) \end{cases} \quad \text{(Hamiltonian equations of motion)} \\ &\begin{cases} \dot S &= L \\ \frac{d}{dt} (\nabla_v L) &= \nabla_q L + (\partial_S L) (\nabla_v L) \end{cases} \quad \text{(Euler–Lagrange equations of motion)} \\ &\begin{cases} dS = \braket{p, dq} - H dt \end{cases} \quad \text{(Hamilton–Jacobi equations)} \\ \end{aligned}

Variational Hamiltonian mechanics

To recap, we have derived two sets of equations: the Euler–Lagrange equations in configuration spacetime, parameterized by (t, q, v), and the Hamiltonian equations in phase spacetime, parameterized by (t, q, p). Both of them came from the same constraint moneymaking scheme:

\begin{cases} \delta \int_{t_0}^{t_1} L(t, q(t), \dot q(t)) dt &= 0 \\ q(t_0) &= q_0, \; q(t_1) = q_1 \end{cases}

This is usually called Hamilton’s principle. However, Hamiltonian’s principle is a statement about trajectories in configuration spacetime, where the variables are just t and q. That is, we are considering only how we, as a factory manager, produce the commodities over time. The market and its prices p do not feature originally in our problem set-up, and the market and its prices are purely a matter of mental accounting.

But what if we do a market reform? Suppose the market really exists, and the prices are as real as steel and concrete? In that case, we enter the realm of phase space-time, where the factory and the market both exist with equal reality, optimizing against each other over time. In this perspective, the variational principle of \delta \int_{t_0}^{t_1} L(t, q(t), \dot q(t)) dt = 0 is unsatisfactory, because only the factory appears explicitly in it, not the market. There is such a statement, called modified Hamilton’s principle:

\begin{cases} \delta \int_{t_0}^{t_1} \braket{p, dq} - H(t, q, p) dt = 0 \\ q(t_0) = q_0, \; q(t_1) = q_1 \end{cases} \tag{1}

Ostensibly, this is “derived” from the Hamilton’s principle by writing \braket{p, dq} = H + L, but this is wrong in two senses. One, the Hamiltonian H is a function of (t, q, p), but the Lagrangian L is a function of (t, q, v). Two, the market is free to vary its price schedule, independently of however the factory might vary its production schedule. In particular, the market can be rampantly mispriced. This is in contrast to the case of \delta \int Ldt, where the market pricing, being a mental accounting technique, is imagined by the factory manager to be ruthlessly efficient.

So let us interpret it anew. It is a new economy, not a planned economy anymore. Let us assume that this is the new economic system:

- There are 3 agents: The government, the market, and the factory.

- The factory sells everything it produces to the market. Thus, the total revenue earned by the factory is \int_{t_0}^{t_1} \braket{p, dq}.

- Meanwhile, the factory is required by the government to pay a form of “rent” to the market. The rent rate is H(t, q, p). In words, the rate of rent depends on time, the total amount of commodity ever produced, and the current market price.

The economy is a kind of zero-sum economy. The factory wants to maximize \int_{t_0}^{t_1} \braket{p, dq} - H dt, while the market wants to minimize it. When neither side can profit from the other side’s mistake by making an infinitesimal variation of its own strategy, we have achieved a (local) Nash equilibrium. This is how we interpret the variational equation \delta\int (\braket{p, dq} - H dt) = 0.

As for the constraints, q(t_0) = q_0 is an initial condition: “The total amount of commodity that has been produced at time t_0 is q_0”. $q(t_0) = q(t_1) = q_1 is a government mandate: The factory must produce exactly q_1 - q_0 during the interval [t_0, t_1]. The market is truly free to vary its commodity pricing, although the government can indirectly control for it by changing the production target for the factory.

Given this, it remains to show that a (local) Nash equilibrium occurs iff the factory and the market follows the Hamiltonian equations.

Wolog, set N = 1. That is, there is only one commodity and one price. Suppose at some moment t \in (t_0, t_1), Hamilton’s equations are violated, then there are 4 possibilities.

If \dot p(t) + \partial_q H > 0, then it means the market is raising the prices too fast right now. The factory can profit by producing less now and pay less rent, and produce more later to exploit the higher price. Specifically, the factory can create a supply shock of -\epsilon q now, wait \delta t, then produce a compensating supply shock of +\epsilon q. The factory’s profit from this double shock is

p(t)(-\epsilon q) + p(t + \delta t)(\epsilon q) - \partial_q H (-\epsilon q)\delta t = (\dot p(t) + \partial_q H)\epsilon q\delta t > 0

If \dot q - \partial_p H > 0, then the factory is producing too fast right now. The market can profit by lowering prices now by \epsilon p and raise it later. The market’s profit from this double shock is

(\partial_p H)(-\epsilon p) \delta t - (-\epsilon p) (\dot q \delta t) = (\dot q - \partial_p H)\epsilon p \delta t > 0

Similarly if \dot p(t) + \partial_q H < 0 or \dot q - \partial_p H < 0.

Thus, if Hamilton’s equations are violated, then we are not at a Nash equilibrium. Conversely, if Hamilton’s equations are satisfied, then no local variation at any point in t \in (t_0, t_1) can be profitable for either side. It remains to handle the case of t = t_0 or t = t_1. In the expression H(t, q, p)dt - pdq, dt = 0 because we are at the end times, and dq = 0 because the factory has quotas to fill, so there is no way to make a profit for either the market or the factory in this case.

The standard proof appearing in (Goldstein, Poole, and Safko 2008, chap. 8) goes like:

- Start with the original system with configuration space (t, q_{1:N}, \dot q_{1:N}).

- Move to the Hamiltonian equations on phase space (t, q_{1:N}, p_{1:N}).

- Regard that as part of a larger system with configuration space (t, q_{1:N}, p_{1:N}, \dot q_{1:N}, \dot q_{1:N})

- Write down the Euler–Lagrange equations for that larger system.

However, this argument only shows that the Hamiltonian equations are necessary for a Nash equilibrium. This is because, to use the Euler–Lagrange equations, we need to fix the end points of q_{1:N}, p_{1:N}. However, this is tantamont to the government simultaneously imposing a production quota on the factory, and fixing the market price at the start and end:

\begin{cases} \delta \int_{t_0}^{t_1} \braket{p, dq} - H(t, q, p) dt = 0 \\ q(t_0) = q_0, \; q(t_1) = q_1\\ p(t_0) = p_0, \; p(t_1) = p_1 \end{cases}

In this economic model, if the government-mandated prices p_0, p_1 are different from what a free market would have picked, then a Nash equilibrium does not exist. For any joint production–pricing schedule, either the factory can exploit the market by infinitesimally modifying the production schedule, or the market can exploit the factory by infinitesimally modifying the pricing schedule. If the government mandates the market to be mispriced at either t_0 or t_1, then at some t \in [t_0, t_1], we must have either \dot p_i + \partial_{q_i} H \neq 0 or \dot q_i - \partial_{p_i} H \neq 0 for some i, creating free money for either the factory or the market.

Exercise 1 Consider the Hamilton–Pontryagin principle, a variational principle in the combined (3n+1)-dimensional configuration-velocity-momentum space-time:

\begin{cases} \delta \int_{t_0}^{t_1} (L(t, q, v) + \braket{p, \dot q - v}) dt = 0 \\ q(t_0) = q_0, \; q(t_1) = q_1 \end{cases}

where \delta v, \delta p are freely variable, and \delta q is freely variable except at the specified end points. Prove that the solution satisfies

\dot{q}=v, \quad p=\frac{\partial L}{\partial v}, \quad \dot{p}=\frac{\partial L}{\partial q}

What does it all mean?

In the Lagrangian formalism, we are given a system with q coordinates, and allowed to manipulate \dot q however we want, in order to minimize a “cost” function \int_0^T L(t, q, \dot q)dt.

In the Hamiltonian formalism, we are also given a market to trade with. We attempt to maximize profit by varying production, buying, and selling. However, the market simultaneously adjusts its prices p in just the right way so that we are always indifferent about the market (if we are ever not indifferent, the market is in serious trouble – it doesn’t actually carry any real commodity!), so we never actually make any trade. The market has been in our heads all along, but its effects are real.

Assuming this kind of double optimization (we against the market, and the market against us), the trajectory is uniquely determined by several possible specifications. We may fix it by (t_0, q_0, p_0), or by (t_0, q_0), (t, q), or by (t_0, q_0, v_0), or perhaps more exotic constraints that mix up t, q, p, v.

Ironically, the Hamiltonian equations of motion flow out naturally in this economic interpretation, with no fuss whatsoever. The Euler–Lagrange equations are derived only as an afterthought. This is exactly backwards compared to the usual way of teaching, where the EL equations are derived first, and the Hamiltonian equations are derived by an unmotivated “Let us define H = \sum_i p_i \dot q_i - L …”, followed by some clumsy and unjustified derivations.

In classical control theory, the price vector p is called “costate” since it is multiplied with the state q, and \dot p= -\nabla_q H is called the “costate equation”. The above methods can be generalized to account for constraints, yielding Pontryagin’s maximum principle, among other results.

The market reform did not change the dynamics of the economy. The market is no longer in the head, but the same Hamiltonian equations of motion reappear. So what is the point of the market reform? The answer is that even though classically, nothing has changed, quantum-mechanically, much has changed. In classical mechanics, momentum is a less real concept than position and velocity, but in quantum mechanics, position and momentum are equally real, while velocity has been demoted to an almost useless concept. So in this sense, the market reform has succeeded, even though we cannot see it from within the classical world.

Cyclic coordinates

Given a system defined by a Lagrangian function L(t, q, v), we say that it is cyclic in the coordinate q_i if L does not depend on q_i. By definition of

H(t, q, p) = \max_v \left(\sum_i p_i v_i - L(t, q, v)\right)

we see that if L does not depend on q_i, then H also does not depend on q_i. Consequently, any optimal trajectory satisfies \dot p_i = -\partial_{q_i} H = 0. That is, p_i is conserved – conservation of generalized momentum.

Routhian mechanics

Suppose that the market does not contain all commodities, but only the last n commodities. That is, let q_{1:N} = (q_{1:s}, q_{s+1:s+n}), and only open markets on q_{s+1:s+n}. The optimal cash flow equation then gives us the “Routhian”:

R(t, q, v_{1:s}, p_{s+1:N}) = \max_{v_{s+1:N}} \left(\sum_{i=s+1}^n p_i v_i - L(t, q, v)\right)

As before, the optimal control variables are v_{s+1:N}^\ast = \mathop{\mathrm{arg\,max}}_{v_{s+1:N}} \left(\sum_{i=s+1}^n p_i v_i - L(t, q, v)\right).

Theorem 4 (Routhian equations of motion) \begin{cases} \partial_t R &= -\partial_t L \\ \frac{d}{dt} \partial_{v_i} R = \partial_{q_i}R \quad & i \in 1:s\\ \begin{cases} \dot q_i = \partial_{p_i} R \\ \dot p_i = -\partial_{q_i} R \end{cases}\quad & i\in s+1:N \end{cases}

By the same argument as in Hotelling’s lemma, we have

\begin{cases} \partial_t R = -\partial_t L \\ \nabla_q R = -\nabla_q L \\ \nabla_{v_{1:s}} R = -\nabla_{v_{1:s}} L \\ \nabla_{p_{s+1 : N}} R = v^*_{s+1 : N} \end{cases}

Plugging the 2-th and 3-th equations into the original Euler–Lagrange equations, we obtain

\frac{d}{dt} \partial_{v_i} R = \partial_{q_i}R \quad i \in 1:s

The 4-th equation gives

\dot q_i =v_i^\ast = \partial_{p_i} R, \quad \forall i\in s+1:N

For i\in s+1:N, we can obtain the price dynamic of the partial market by the no-arbitrage condition, giving

\dot p_i = \partial_{q_i} L = -\partial_{q_i} R

We see that the first s equations look just like the EL equations, but the next 2n equations look just like the Hamiltonian equations. The Routhian equations make an awkward hybrid.

… as a fundamental entity, the Routhian is a sterile hybrid, combining some of the features of both the Lagrangian and the Hamiltonian pictures. For the development of various formalisms of classical mechanics, the complete Hamiltonian formulation is more fruitful.

Application to cyclic coordinates

Though the Routhian equations are theoretically useless, they are useful for solving specific problems. For some worked examples of using the Routhian, see the Wikipedia page.

While the Euler–Lagrangian equations are N second-degree differential equations, the Hamiltonian equations are 2N first-degree differential equations. We are essentially trading derivatives for equation numbers.

Though the EL equations and the Hamiltonian equations are philosophically different, for solving particular problems, they often end up giving the same equations anyway. Specifically, if we are solving the Hamiltonian equations for a concrete example, by eliminating the variables p, we often end up right back to the Euler–Lagrange equations. This would be quite the detour, and if there are cyclic coordinates, the Routhian could save us some trouble.

If we have a system that is cyclic in the last n coordinates, then since \nabla_q R = -\nabla_q L, its Routhian satisfies \partial_{q_i} R = 0 for the last n coordinates too. Then we find that the Routhian equations become:

\begin{cases} \frac{d}{dt} \partial_{v_i} R = \partial_{q_i}R \quad & i \in 1:s\\ \begin{cases} \dot q_i = \partial_{p_i} R \\ p_i = p_i(0) \end{cases}\quad & i\in s+1:N \end{cases}

giving us n first-degree equations and N-n second-degree equations. If we were to start with the Hamiltonian equations of motion, we would get

\begin{cases} \dot q_i = \partial_{p_i} H \\ p_i = p_i(0) \end{cases}\quad i\in s+1:N

by the same reasoning, and then laboriously eliminate the variables p_i for i \in 1:s, and end up with s second-degree differential equations, often exactly the same as the first s Routhian equations:

\frac{d}{dt} \partial_{v_i} R = \partial_{q_i}R \quad i \in 1:s

This is how the Routhian saves us some effort in practical calculations. It is useful in this way, and in this way only.

Bonus: Higher-order Lagrangians and Hamiltonians

What happens if we use a Lagrangian with higher-order derivatives? It turns out that even in this case, we can still use economic reasoning to derive its Hamiltonian and Euler–Lagrangian equations

Exercise 2 Read the following sections, then generalize the derivation to n-th-order derivatives.

This construction of Hamiltonians from higher-order Lagrangians is often called Ostrogradsky theorem or Ostrogradsky instability, because Ostrogradsky published it in 1850 (Ostrogradsky 1850) after seeing Hamilton’s paper of 1833 (Hamilton 1833). He did not note its implications for instability, which was first noted by Pais and Uhlenbeck in 1950 (Pais and Uhlenbeck 1950). For this reason, it’s also called the Pais–Uhlenbeck model.

When Lagrangian also depends on acceleration

When the Lagrangian depends not just on position and velocity, but also acceleration, the total cost to be optimized is:

S(q) := \int L(t, q^{(0)}, q^{(1)}, q^{(2)})dt

where q^{(n)} is a symbol that suggests itself to be the n-th time-derivative of the optimal trajectory q, although it is actually defined for any tuple of real numbers, even when we don’t have q^{(1)}(t) = \frac{d}{dt}q^{(0)}(t).

Our previous method, which is to open a market on position q, fails for two reasons:

- The producer cannot optimize its velocity, because now velocity is no longer a control variable. Now, both position and velocity are state variables, and only acceleration is a control variable.

- The producer cannot buy and sell velocity, so it has no price signal to optimize its acceleration (how fast it produces velocity).

If the market fails, make it bigger: allow the market to buy and sell not just position, but also velocity.

We open a market of both positions and velocities. The price vector of positions is p^{(0)} and the price vector of velocities is p^{(1)}. Then, the maximal profit flow is

H(t, q^{(0)}, q^{(1)}, p^{(0)}, p^{(1)}) = \max_{ q^{(2)}} (\langle p^{(0)} , q^{(1)}\rangle + \langle p^{(1)} , q^{(2)}\rangle - L(t, q^{(0)}, q^{(1)}, q^{(2)}))

and the optimal production plan is

q^{(2)\ast} = \mathop{\mathrm{arg\,max}}_{ q^{(2)}}(\langle p^{(0)} , q^{(1)}\rangle + \langle p^{(1)} , q^{(2)}\rangle - L)

Hamiltonian equations

We can prove the Hotelling’s lemma for this Hamiltonian, using the same no-arbitrage argument as before:

\begin{cases} \partial_t H = -\partial_t L \\ \nabla_{q^{(0)}} H = -\nabla_{q^{(0)}} L \\ \nabla_{q^{(1)}} H = p^{(0)}-\nabla_{q^{(1)}} L \\ \nabla_{p^{(0)}} H = q^{(1)} \\ \nabla_{p^{(1)}} H = q^{(2)\ast} \end{cases}

Along an optimal trajectory, the producer always chooses \dot q^{(1)} = q^{(2)\ast}, and has no choice in \dot q^{(0)} = q^{(1)}, so we have two equations of motion:

\begin{cases} \dot q^{(1)} = q^{(2)\ast} = \nabla_{p^{(1)}} H\\ \dot q^{(0)} = q^{(1)} = \nabla_{p^{(0)}} H \end{cases}

The market must adjust its prices by the no-arbitrage condition, as before. If we inflict a position shock of \delta q^{(0)}, then by no-arbitrage, selling it now or later is equally (up to order \delta^2) profitable:

\langle p^{(0)} , \delta q^{(0)}\rangle = \langle p^{(0)} + \dot p^{(0)} \delta t , \delta q^{(0)}\rangle - \langle \nabla_{q^{(0)}} L , \delta q^{(0)}\rangle \delta t

yielding \dot p^{(0)} = \nabla_{q^{(0)}} L = -\nabla_{q^{(0)}} H.

For the last equation of motion, inflict a velocity shock of \delta q^{(1)}. The effect of the shock include both its effect on q^{(0)} and L, thus the no-arbitrage equation states:

\underbrace{\langle p^{(1)} , \delta q^{(1)}\rangle}_{\text{selling now}} = \underbrace{\langle p^{(1)} + \dot p^{(1)} \delta t , \delta q^{(1)}\rangle}_{\text{selling later}} + \underbrace{\langle p^{(0)} + \dot p^{(0)} \delta t , \delta q^{(1)}\delta t\rangle}_{\text{profit from extra }p^{(0)}} - \underbrace{\langle \nabla_{q^{(1)}} L , \delta q^{(1)}\rangle \delta t}_{\text{cost from holding extra }p^{(1)}}

which yields the last equation \dot p^{(1)} = \nabla_{q^{(1)}} L - p^{(0)} = -\nabla_{q^{(1)}} H.

In summary, we have

Theorem 5 (higher-order Hamiltonian equations of motion:) \begin{cases} \dot q^{(1)} = \nabla_{p^{(1)}} H\\ \dot q^{(0)} = \nabla_{p^{(0)}} H \\ \dot p^{(0)} = -\nabla_{q^{(0)}} H \\ \dot p^{(1)} = -\nabla_{q^{(1)}} H \end{cases}

Euler–Lagrange equations

In order to obtain the Euler–Lagrange equations of motion, we need to work backwards from the Hamiltonian equations of motion as before.

From the Hamiltonian, we can go back to the Lagrangian by inverting the convex transform:

L(t, q^{(0)}, q^{(1)}, q^{(2)}) = \max_{p^{(0)} ,p^{(1)}} (\langle p^{(0)} , q^{(1)}\rangle + \langle p^{(1)} , q^{(2)}\rangle - H(t, q^{(0)}, q^{(1)}, p^{(0)}, p^{(1)}))

Here we are given a hint of the troubles ahead. Since H is linear in p^{(1)}:

H(t, q^{(0)}, q^{(1)}, p^{(0)}, p^{(1)}) = \langle p^{(0)} , q^{(1)}\rangle + \max_{ q^{(2)}} (\langle p^{(1)} , q^{(2)}\rangle - L(t, q^{(0)}, q^{(1)}, q^{(2)}))

there is no way to fix p^{(1)} in the inverse transform! In detail, we plug the equation for H into the equation for L, to get

L(t, q^{(0)}, q^{(1)}, q^{(2)}) = \max_{p^{(0)} ,p^{(1)}} (\langle p^{(1)} , q^{(2)}\rangle - \max_{ q^{(2)}} (\langle p^{(1)} , q^{(2)}\rangle - L(t, q^{(0)}, q^{(1)}, q^{(2)}))

and we see that there is no optimality constraint on p^{(0)}. This is a hint of instabilities ahead.

Differentiating L, we get

\begin{cases} \partial_t L = -\partial_t H\\ \nabla_{q^{(0)}}L = -\nabla_{q^{(0)}}H \\ \nabla_{q^{(1)}}L = p^{(0)} - \nabla_{q^{(1)}}H \\ \nabla_{q^{(2)}}L = p^{(1)\ast} \end{cases}

Now, along the optimal trajectory, we must have \nabla_{q^{(2)}}L = p^{(1)\ast}, so taking its time-derivative, we get

\frac{d}{dt}\nabla_{q^{(2)}}L = \dot p^{(1)} = -\nabla_{q^{(1)}}H = \nabla_{q^{(1)}}L - p^{(0)}

Take another time-derivative, to obtain the Euler–Lagrange equations of motion:

\sum_{i=0}^2\left(-\frac{d}{d t}\right)^i (\nabla_{q^{(i)}} L ) =0

The generalization to L(t, q^{(0)}, ..., q^{(N-1)}) is immediate. It can be derived by a similar argument through the market economy.

Ostrogradsky instability and the anthropic principle

Thus, we see that the entire machinery of Lagrangian and Hamiltonian mechanics still apply. In particular, we have a Hamiltonian:

H(t, q^{(0)}, q^{(1)}, p^{(0)}, p^{(1)}) = \langle p^{(0)} , q^{(1)}\rangle + \max_{ q^{(2)}} (\langle p^{(1)} , q^{(2)}\rangle - L(t, q^{(0)}, q^{(1)}, q^{(2)}))

But now we have a catastrophe. Consider an oscillator with higher-order derivatives. Since its Hamiltonian contains a term \langle p^{(0)} , q^{(1)}\rangle, it is linear with respect to p^{(0)} and q^{(1)}. In other words, it can have arbitrarily low energy states.

Now, this could be alright if we live in a classical world, but we live in a world described by quantum field theory. In QFT, the world is a giant network of oscillators. If a quantum oscillator has higher-order derivatives, then its energy levels can go both infinitely high and low. If there is any coupling at all between its energy levels, it would instantly evaporate into infinitely many positive and negative energy particles, in a blaze of vacuum decay.

This is an anthropic explanation for “Why Newton’s laws?” Newton’s laws, because the Lagrangian depends on only up to velocity. Why? Because if it also depends on acceleration, the vacuum would decay (Swanson 2022). We can similarly explain anthropically why space has 3 dimensions, and time has 1 dimension.

With more or less than one time dimension, the partial differential equations of nature would lack the hyperbolicity property that enables observers to make predictions. In a space with more than three dimensions, there can be no traditional atoms and perhaps no stable structures. A space with less than three dimensions allows no gravitational force and may be too simple and barren to contain observers.

(Tegmark 1997).

An unstable higher-order oscillator

It is beyond our scope to quantitatively discuss Ostrogradsky instability in quantum field theory, however, we can have a taste of it here. Consider the oscillator perturbed by \epsilon:

L = \frac 12 m\dot x^2 - \frac 12 kx^2 - \frac 12 \epsilon \ddot x^2

Its EL equation is

\epsilon x^{(4)} + m\ddot x + kx = 0

a linear order-4 equation, so its solutions are of the form x = \sum_{i=1}^4 a_i e^{z_i t}, where z_1, z_2, z_3, z_4 are its fundamental (complex) frequencies. Plug them in the equation and solve it simply:

z = \pm \sqrt{-\frac{1}{2\epsilon} (m \pm \sqrt{m^2 - 4\epsilon k})}

At small |\epsilon| limit, we have

z \approx \pm i\sqrt{\frac km}, \pm\sqrt{-\frac m\epsilon}

and so if \epsilon < 0, one of the modes is exponentially growing at rate \sqrt{m/|\epsilon|}.

If \epsilon > 0, then the oscillator survives, with two modes of oscillation of frequency \sqrt{\frac km} and \sqrt{\frac{m}{\epsilon}}. When there is viscous force, however, this delicate stability is destroyed. (Nesterenko 2007)

The equation of motion in this case is

\epsilon x^{(4)} + m\ddot x + \gamma \dot x + kx = 0

Let the ansatz be e^{i\omega t}, the algebraic equation to solve is now \epsilon \omega^4 - m\omega^2 + i\gamma \omega + k = 0. At the small \gamma limit, the perturbative solution \omega = \pm\sqrt{\frac{m}{\epsilon}} + \delta yields \delta = \mp i \frac{\gamma}{2m}. Thus, we see that the \sqrt{\frac{m}{\epsilon}} mode of oscillation splits into two sub-modes: an exponentially decaying mode and an exponentially growing mode, both at the rate of \frac{\gamma}{2m}.

Similarly, the perturbative solution \omega = \pm\sqrt{\frac{k}{m}} + \delta shows that the \sqrt{\frac{k}{m}} mode of oscillation also splits in the exact same way: an exponentially decaying mode and an exponentially growing mode, both at the rate of \frac{\gamma}{2m}.

Interpreted in quantum field theory, this means that the oscillator, with even the slightest mutual interaction between its +\sqrt{\frac{k}{m}} and -\sqrt{\frac{k}{m}} modes, will cause an exponential growth of one of the modes. A catastrophic explosion of particles!

The quantum field theorists call these “bad Ostrogradsky ghosts”, and spend some effort in removing them. Bad ghosts cannot be allowed, because bad ghosts will destroy the universe. Mutual interaction must be preserved between oscillation modes, because nothing is completely independent in this universe – even photons can interact. Some theorists thus simply declare higher-than-2 derivatives forbidden, while others do some renormalization-exorcism, and so on.

Hamilton–Jacobi equation

Hamilton’s principal function

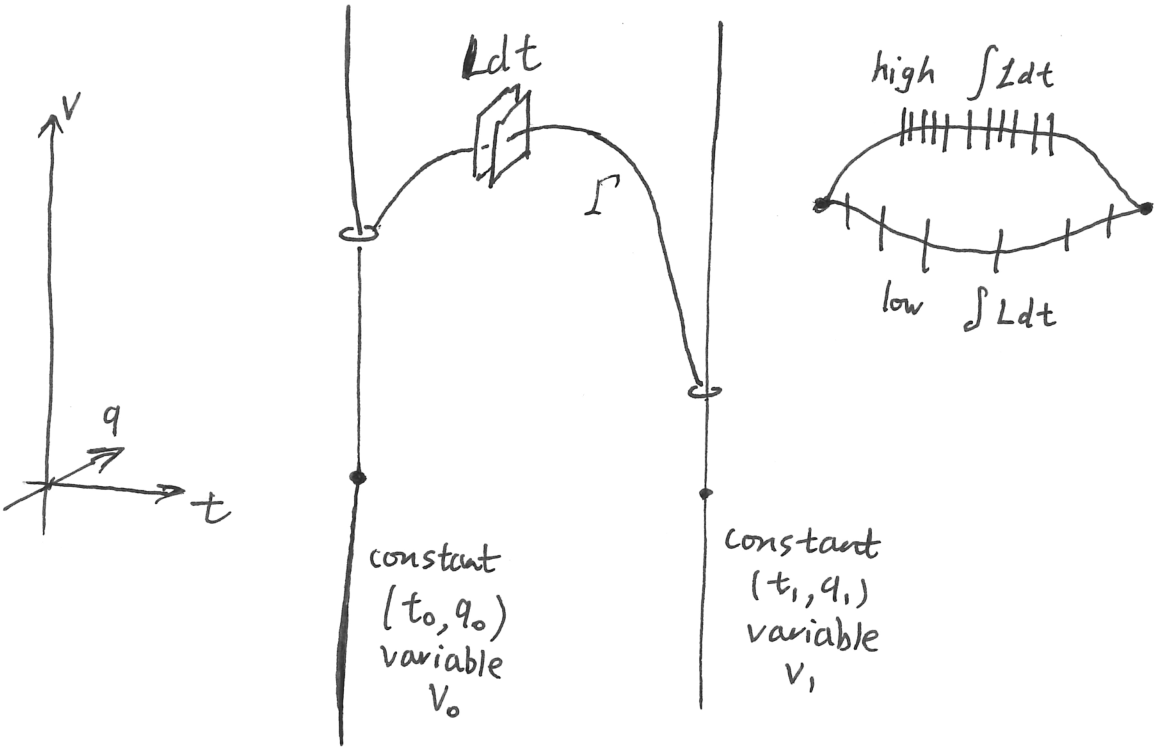

Consider a problem in traveling: Given a starting spacetime (t_0, q_0) and an ending spacetime (t, q), what is the lowest cost of traveling between them? We want to define it as:

S(t, q; t_0, q_0) = \int_{t_0}^t L(\tau, \gamma(\tau), \dot\gamma(\tau))d\tau

where \gamma is the path from (t_0, q_0) to (t, q). However, we have a problem. Do you see it?

Each trajectory \gamma, physically real or physicall unreal, has a cost \int_\gamma Ldt. The cost is well-defined. Now I ask you: if we fix the starting point (t_0, q_0) and the ending point (t, q), what is the cost of going from (t_0, q_0) to (t, q)? Hold on. Don’t get excited. There is a serious issue here! Can you see it?

Let’s assume the earth is a perfect sphere. You need to go from London to Paris in 1 day, and you must travel at constant velocity. Alright, you will travel at a constant speed of 14 km/h in that direction – but hold on! You could also travel at 1681 km/h in the same direction, pass Paris, around the earth, pass London, and stop at Paris. That may sound silly, but remember that classical mechanics specifically does not care about finding the globally best path, only the locally stationary path. You can go around the earth an arbitrary number of times. All these paths are stationary!

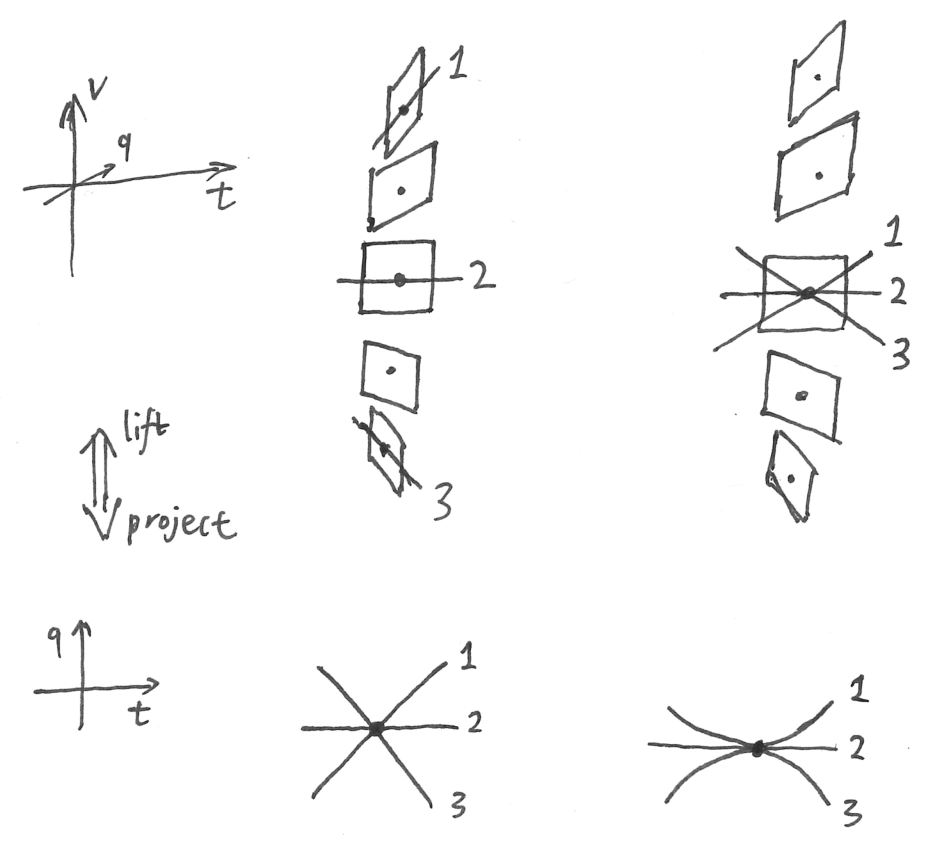

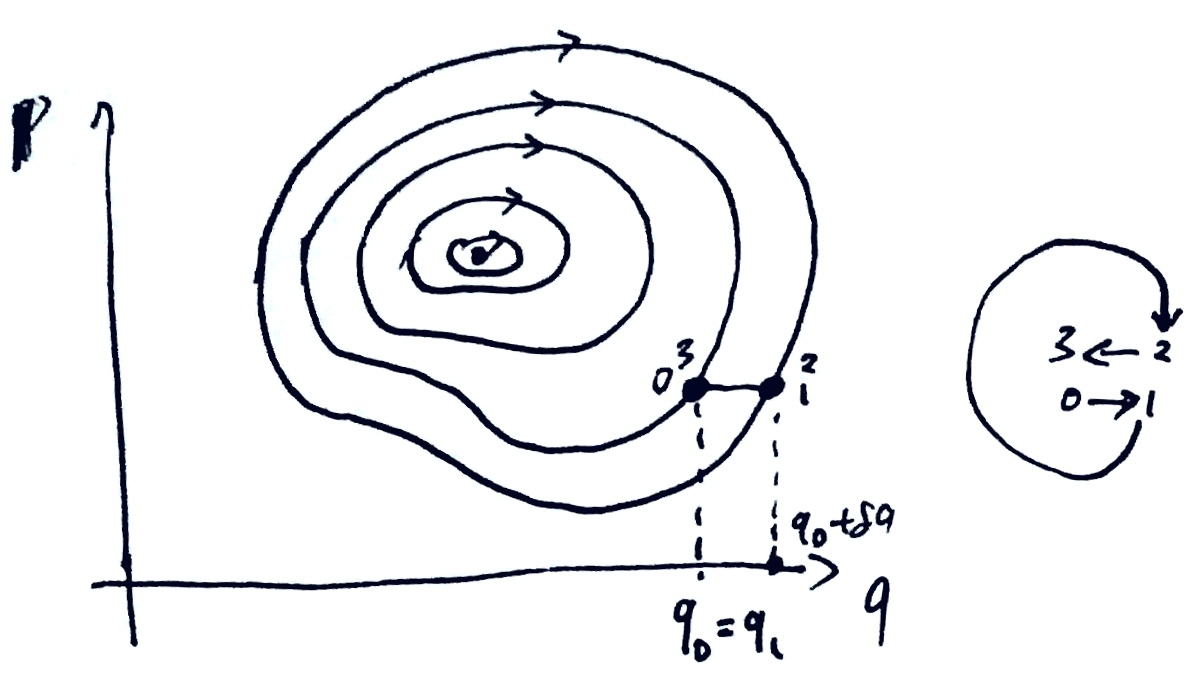

In general, given any two points (t_0, q_0), (t, q), there can be infinitely many paths that connect both points. Therefore, we cannot say “the path” (t_0, q_0) to (t, q). We can only say “a path”. So how do we define S(t, q; t_0, q_0) now?

Looking at the earth-traveling problem again, we notice something: Even though there are infinitely many ways to stationarily go from London to Paris, they are well separated from each other. You cannot slightly change your travel plan, and suddenly find yourself going around the earth one more round. This saves our definition of S. As follows:

First, we select a prototypical path \tilde\gamma Next, we smoothly vary \tilde\gamma until it becomes some path \gamma that goes from (t_0, q_0) to (t, q). Finally, define the Hamilton’s principal function using this particular \gamma. The construction is a bit awkward, but it would allow us to avoid the non-uniqueness problem.

Thus, we define the Hamilton’s principal function:

S(t, q; t_0, q_0) = \int_{t_0}^t L(\tau, \gamma(\tau), \dot\gamma(\tau))d\tau \tag{2}

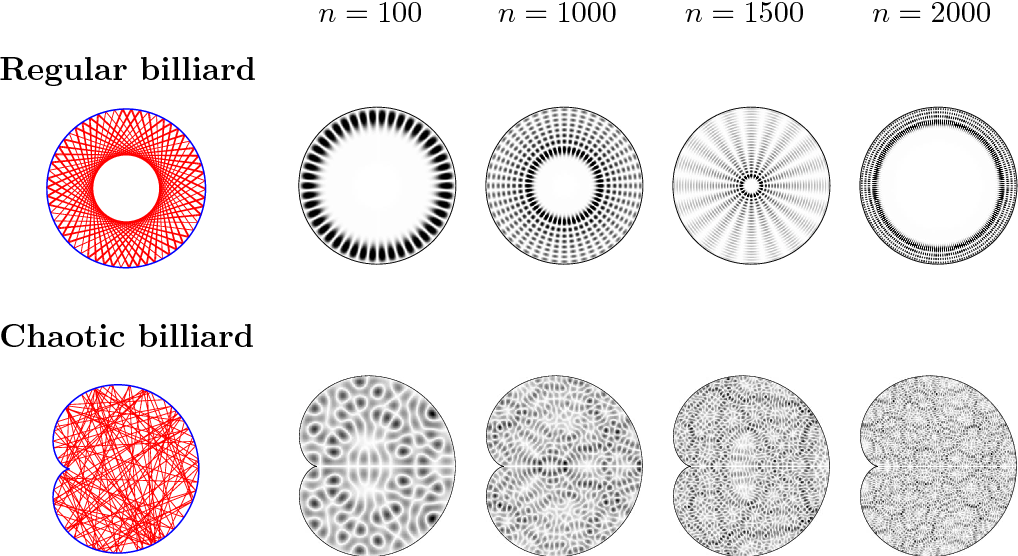

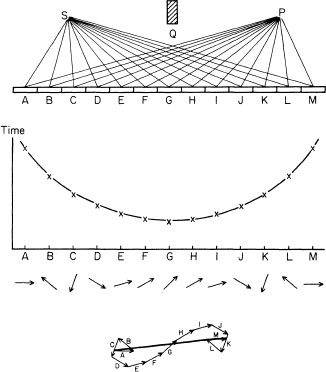

Billiards in a circular board

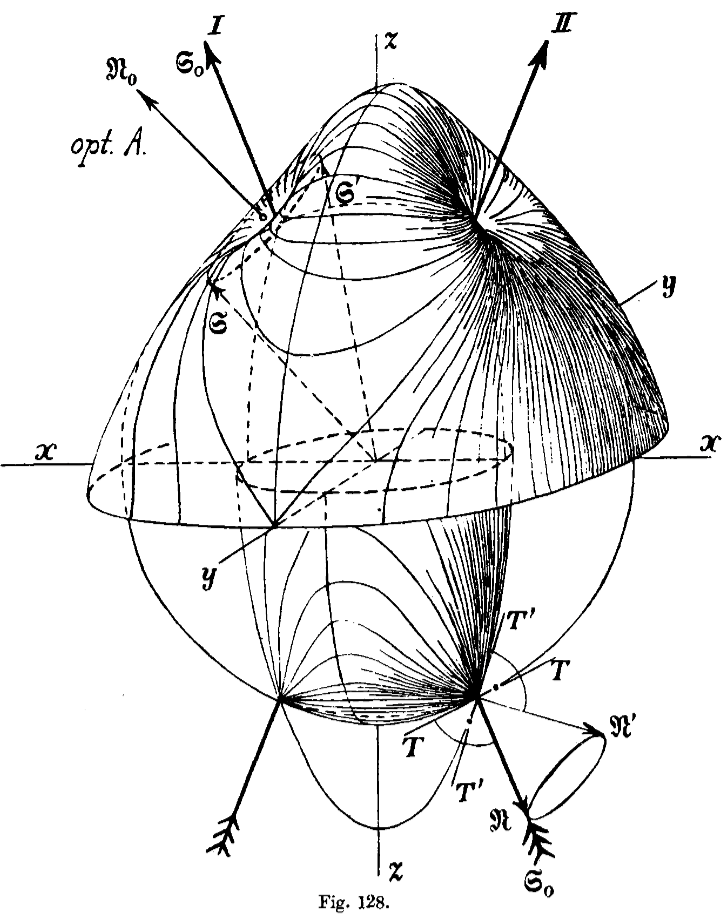

To be more concrete, consider a billiard ball in a circular table.

When both q_0, q are the center of the billiard table, then there are S^1 \times \mathbb{N} ways to go from q_0 to q over the interval [t_0,t]. Here, S^1 denotes the circle of possible directions, and \mathbb{N} denotes the discrete number of starting speeds: \frac{2R}{t-t_0}, \frac{4R}{t-t_0}, \dots.

When not both of them are in the center, then there are only in general \mathbb{N} ways to go from q_0 to q over the interval [t_0,t].

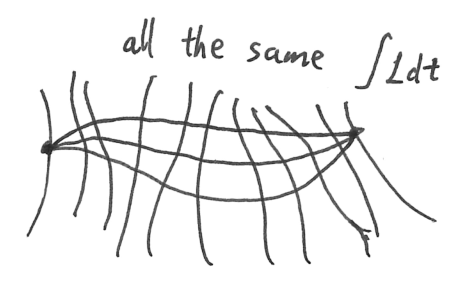

Consider a billiard ball in a circular (not elliptical) table. Let q, q_0 be any two points inside the table, not both on the center, and t_0 < t be two moments in time, then there are a countable infinity of possible trajectories that reach (t, q) from (t_0, q_0).

There are two ways to see this visually, a particle way and a wave way.

For the particle way, define:

- the billiard’s starting angle is \theta, with \theta chosen such that when \theta = 0, the billiard would move on a diameter of the table.

- l(\theta, n) is the oriented line segment that starts at the point where the billiard’s hits the table for the n-th time, and ends at the point where it hits for the (n+1)-th time.

For any n = 1, 2, ..., as \theta moves from \theta = 0 to \theta = \pi, the line l(\theta, n) smoothly varies from the diameter in one direction to the diameter in the opposite direction. Now, if you take a diameter in the circle, and smoothly turn it around by 180^\circ, then no matter how much you shift the line around in the mean time, you are forced to sweep it over every point at least once.4 Consequently, every point can be reached after n reflections, for any positive integer n

4 If you want a hands-on approach, imagine hammering in a nail at some point q in the circle, and putting a long stick on the diameter. Now grab the stick and start turning it around. There is no way for you to turn it by 180^\circ without hitting the nail at some time.

For the wave way, imagine simultaneously shooting out a billiard in every direction with constant speed, and watch the “wavefront” of billiards evolve. The wavefront is reflected by the table edges and assumes increasingly complicated shapes, but it remains a closed curve (with possible self-intersections). As the closed curve reverberates across the table again and again, it sweeps across every point in the table again and again at discrete intervals.

However, there is no way to smoothly reach one trajectory from any other – you either have to make a discrete jump in how hard you strike the billiard ball, or in which direction you strike. This contrasts with the case with both q, q_0 at the center, where you can smoothly vary your striking angle while keeping the same striking force.

Similarly, for a table with smooth boundary, for almost all point-pairs in the table, there are also a countable infinity of trajectories between them. We must say “almost all” to exclude singular cases such as the two focal points of an ellipse, where there is a whole continuum of trajectories between them.5

5 Exactly counting the singular cases, and studying polygonal, or even non-convex tables, is an ongoing research program, with the name of “dynamical billiard flow”.

What is the general lesson for defining S? In general, we need to do two things:

- Fix a particular optimal path \tilde\gamma, and only consider optimal paths that can be reached by continuously deforming that path. This is the same idea as selecting a branch cut when dealing with multi-valued functions like the complex logarithm.

- Avioid hitting the special points. To study the cost of traveling on a sphere, we must avoid our antipodal point. In general, we must avoid the points that can be reached by trajectories that are “too stationary”, because as soon as we hit those points, we break single-valuedness.6

6 How stationary is “too stationary”? We want trajectories that are as stationary as x=0 in y = x^2, but not too stationary like x=0 in y=x^3, or even y=x^4. This has deep connections to catastrophe theory and the theory of caustics, but it will take us too far afield to write it out.

Why are we so concerned with reflections? Why does this feel like geometric optics? Read on!

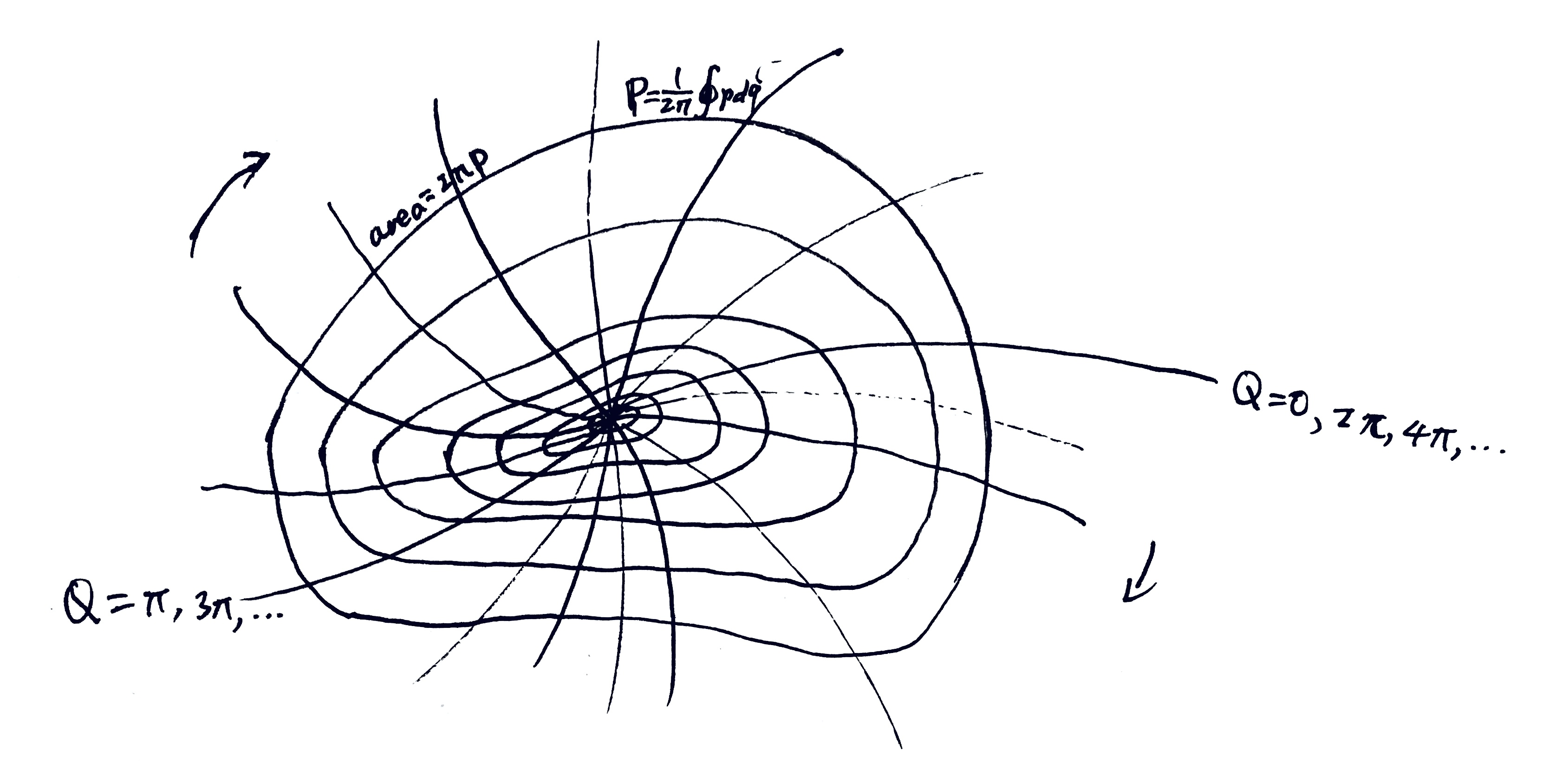

Hamilton–Jacobi equation

For all nice enough Lagrangian L, Hamilton’s principal function S is differentiable with respect to (t, q), so we will study its differential equation.

Let’s first consider the easy case: we simply let the trajectory “run a little longer”. That is, we let the trajectory run from (t_0, q_0) to (t, q), then let it keep running for \delta t, reaching (t+\delta t, q + \delta q). It’s clear that we have \delta q = \dot q(t) \delta t, and

S(t+\delta t, q + \delta q; t_0, q_0) - S(t, q; t_0, q_0) = \left(\sum_i p_i \dot q_i - H\right)\delta t

so we have:

\partial_t S + \sum_i \partial_{q_i}S \dot q_i = - H + \sum_i p_i \dot q_i \tag{3}

which strongly suggests

Theorem 6 (-\partial_t, \nabla_q)S(t, q; t_0, q_0) = (H, p), \quad (-\partial_{t_0}, \nabla_{q_0})S(t, q; t_0, q_0) = (-H_0, -p_0) \tag{4}

If we consider only the t, q part of S, we have a more elegant differential form:

dS = \braket{p, dq} - Hdt \tag{5}

If Equation 4 is indeed true, then we have

Theorem 7 (Hamilton–Jacobi equation) \partial_t S + H(t, q, \nabla_q S) = 0

It suffices to prove \nabla_q S = p, since then \partial_t S = -H follows from Equation 3.

It suffices to prove (-\partial_t, \nabla_q)S(t, q; t_0, q_0) = (H, p), since the other one is proved by the same argument, time-reversed.

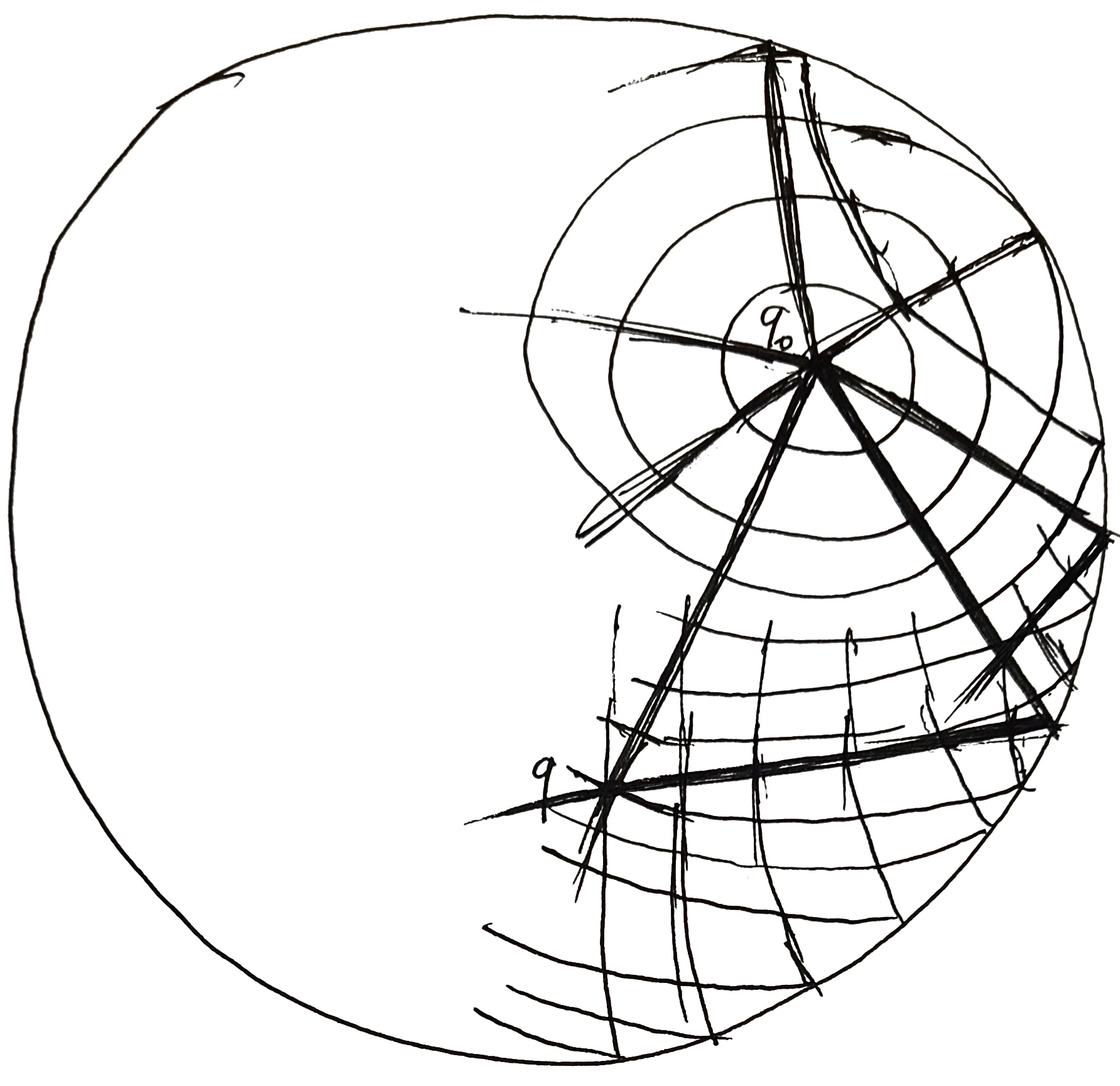

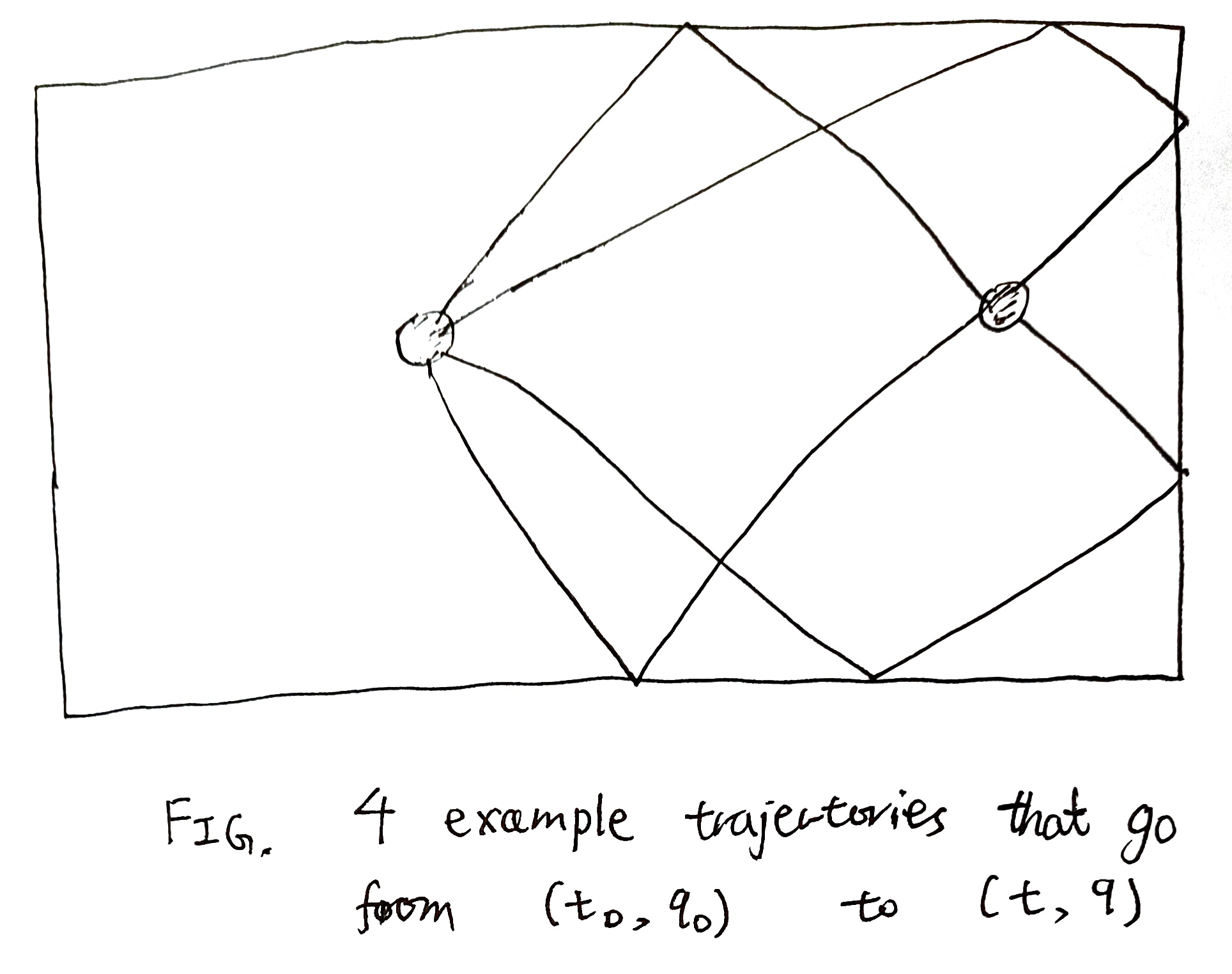

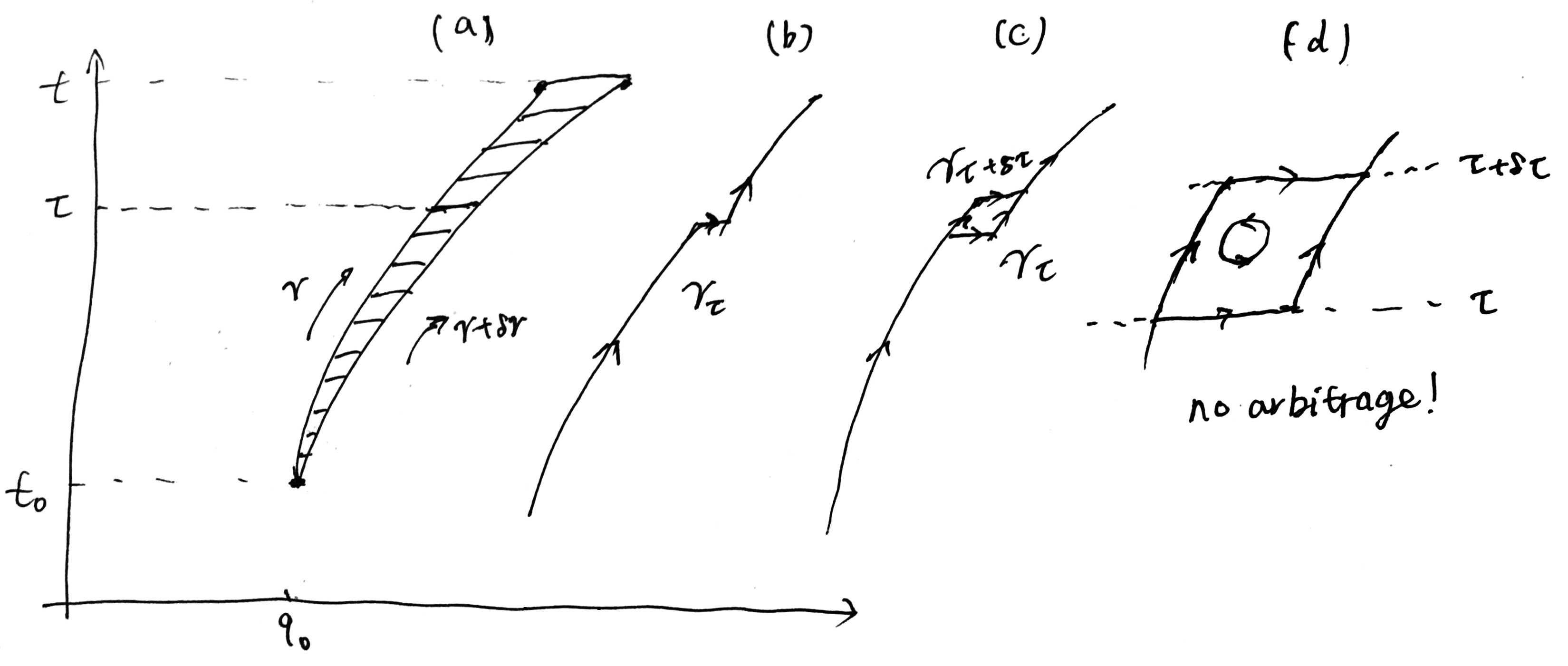

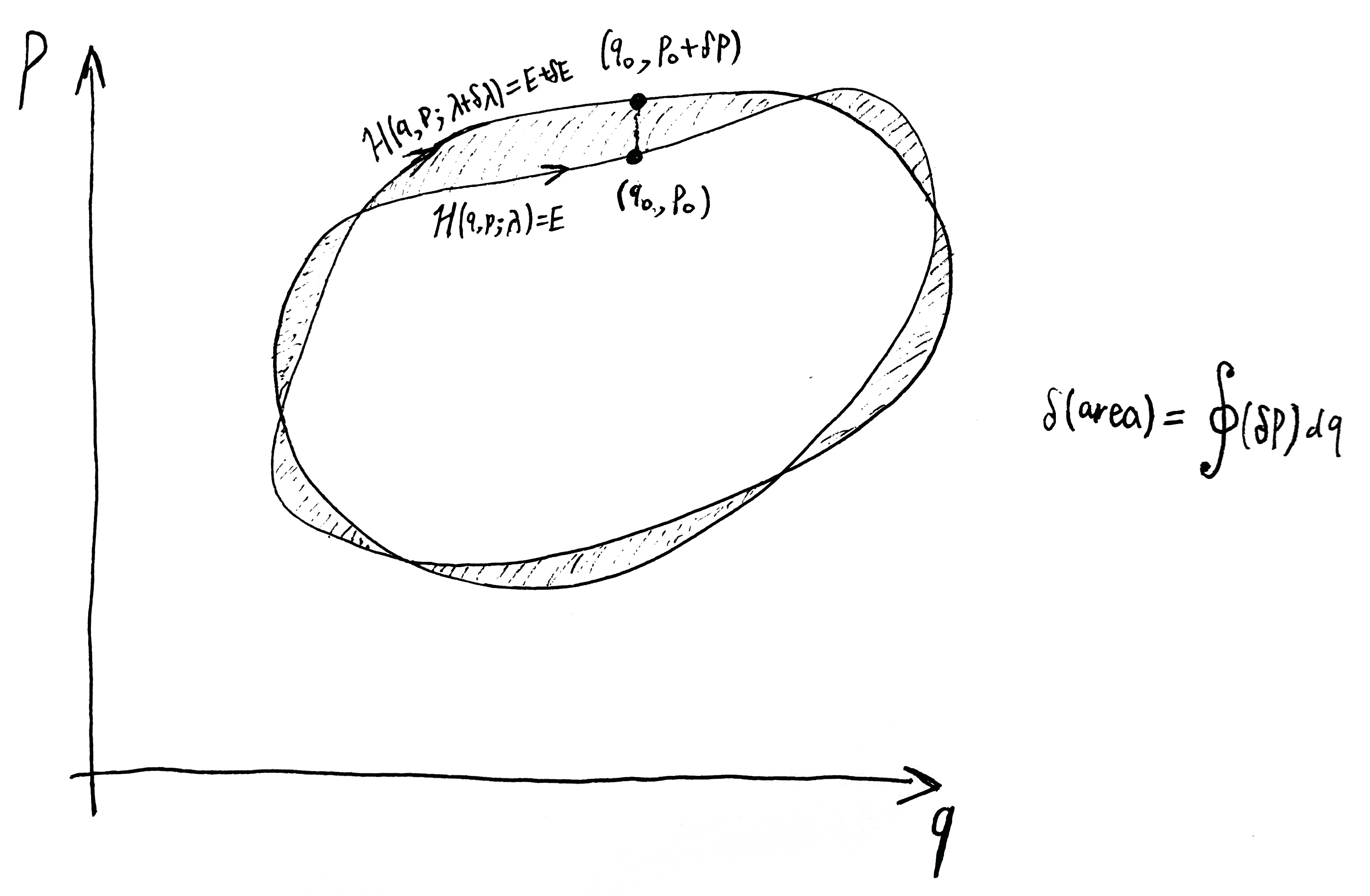

Recall the economic construction of p. It is a price vector designed specifically to destroy all arbitrage opportunities. Consequently, we can consider an entire family of paths shown in Figure (a, b).

Here, \gamma is the path from (t_0, q_0) to (t, q), and \gamma + \delta \gamma is the path to (t, q+\delta q). We interpolate between them by a family of paths \{\gamma_\tau\}_{\tau}, where \gamma_\tau is the path obtained by first moving on \gamma for time t\in [t_0, \tau], then making a “jump” by “purchasing from the market”7 an infinitesimal bundle of commodities so that we fall onto the \gamma + \delta \gamma path, then continue along that path.

7 We are using the market for real now, so the marketeer had better had stocked up on those commodities!

8 More precisely, a higher-order infinitesimal than the area of the parallelogram. See Tip 1.

Now consider two such jumped-paths, \gamma_{\tau} and \gamma_{\tau + \delta \tau}, where \delta \tau is an infinitesimal, shown in Figure (c). The cost difference between them is that between two sides of the parallelogram. By the no-arbitrage construction, the difference is zero.8

Thus, we can smoothly “glide”9 the path \gamma to \gamma + \delta\gamma by the family of jumped-paths \gamma_\tau, with \tau going from t to t_0, with no change in cost.10 Thus, the only cost difference between \gamma and \gamma + \delta \gamma is the cost it takes to buy the bundle of commodities \delta q at the very last instance:

9 In the jargon of topology, this is a homotopy of paths.

10 More precisely, their difference in cost is a higher-order infinitesimal than the area of the curvy triangle between them. Since the curvy triangle is an infinitesimal of order \delta q, the difference in cost is a higher-order infinitesimal than \delta q.

S(t, q+\delta q; t_0, q_0) - S(t, q; t_0, q_0) = \sum_i p_i \delta q_i

finishing the proof.

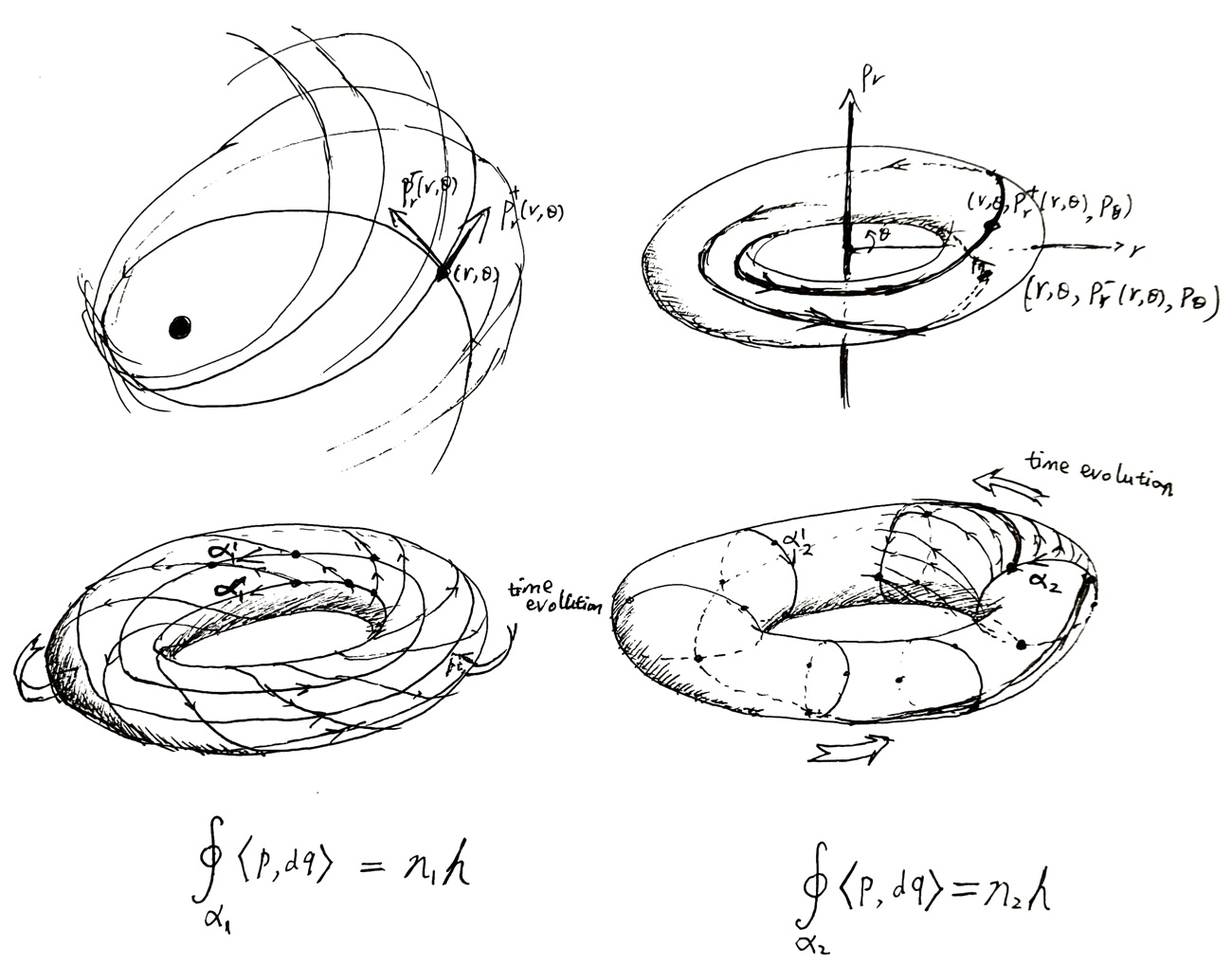

Theorem 8 (Poincaré–Cartan integral invariant (Arnolʹd 2001, 237–38)) Draw an arbitrary closed cycle \alpha in phase space-time. Let every point A \in \alpha evolve for some time (not necessarily the same amount of time) to reach some other point A'. Let \alpha' be the cycle consisting of those points A'. Then we have the Poincaré–Cartan integral invariant

\oint_\alpha \left\langle p, dq\right\rangle - Hdt = \oint_{\alpha'} \left\langle p, dq\right\rangle - Hdt

As a special case, if both \alpha and \alpha' consists of simultaneous points, then it reduces to the Poincaré relative integral invariant

\oint_\alpha \left\langle p, dq\right\rangle = \oint_{\alpha'} \left\langle p, dq\right\rangle

By the HJE, this is equivalent to \oint_{\alpha - \alpha'} dS = 0, which is just Stokes’s theorem.

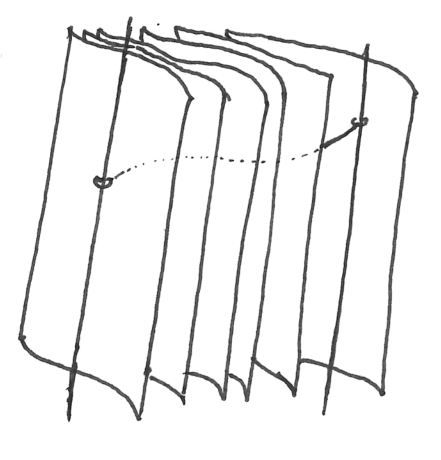

But this is too slick, so we prove it again by drawing pictures. Divide the tube into ribbons, like a barrel, then note that the integral around each barrel-plank is zero, as argued before.

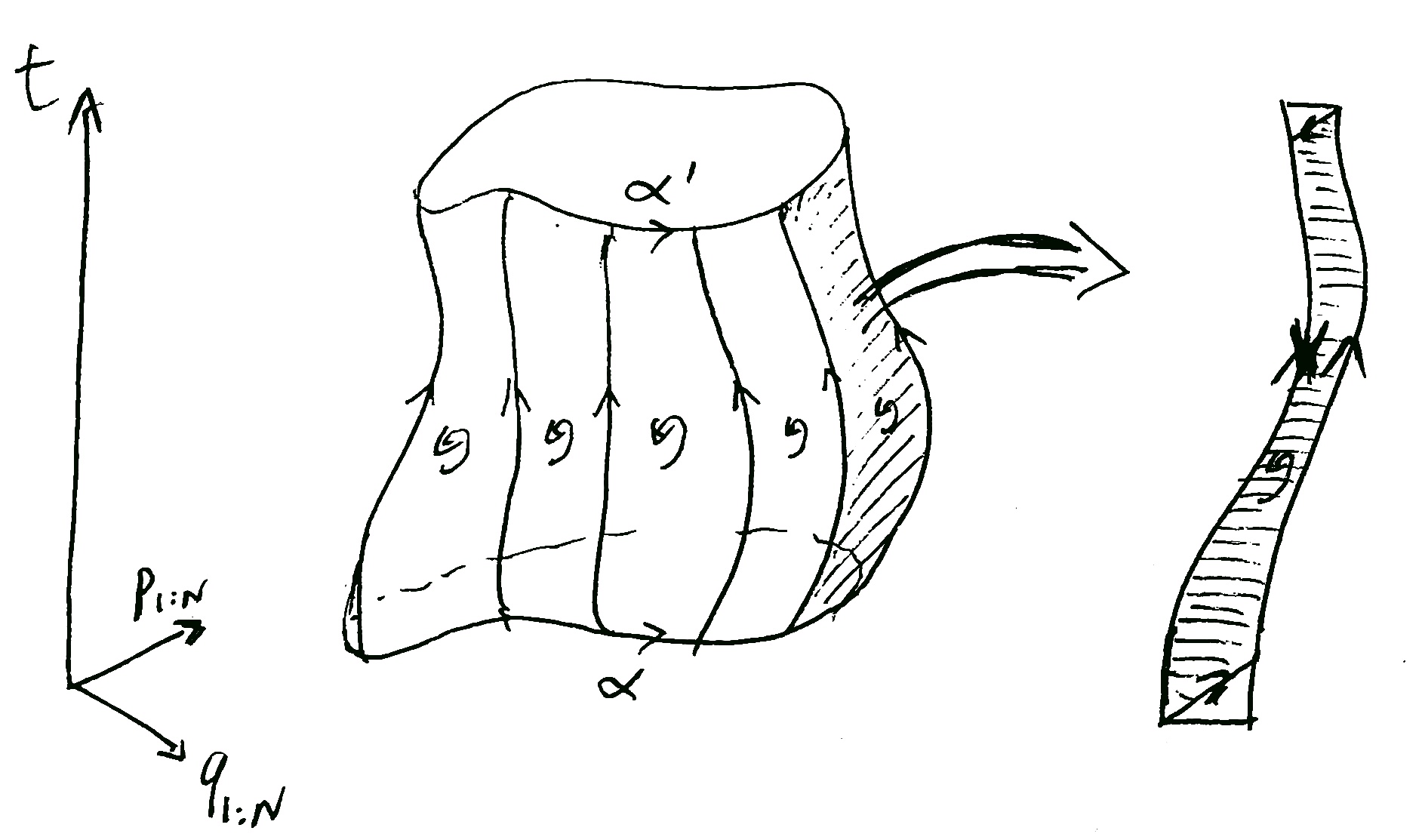

In more detail, we can consider the four ends of a barrel-plank parallelogram. Label those points as A, B, A', B' as shown. Though the points A, B, A', B' exist in phase space-point, we can forget their momenta, thus projecting them to configuration space-time. Each phase space-time trajectory projects to a trajectory in configuration space-time, and we obtain S_{A \to B} = S(t_A, q_A; t_B, q_B), etc.

Now, by Equation 4, we can shift S_{A \to B} to S_{A \to B'}, then to S_{A' \to B'}:

S_{A \to B} = S_{A \to B'} -H_B \delta t_B + \left\langle p_B , \delta q_B\right\rangle = S_{A' \to B'} + H_A \delta t_A - \left\langle p_A , \delta q_A\right\rangle -H_B \delta t_B + \left\langle p_B , \delta q_B\right\rangle

Now, if we shift around one entire cycle, we would get back the same S_{A \to B}. Thus the two integrals are equal.

We will prove Noether’s theorem similarly.

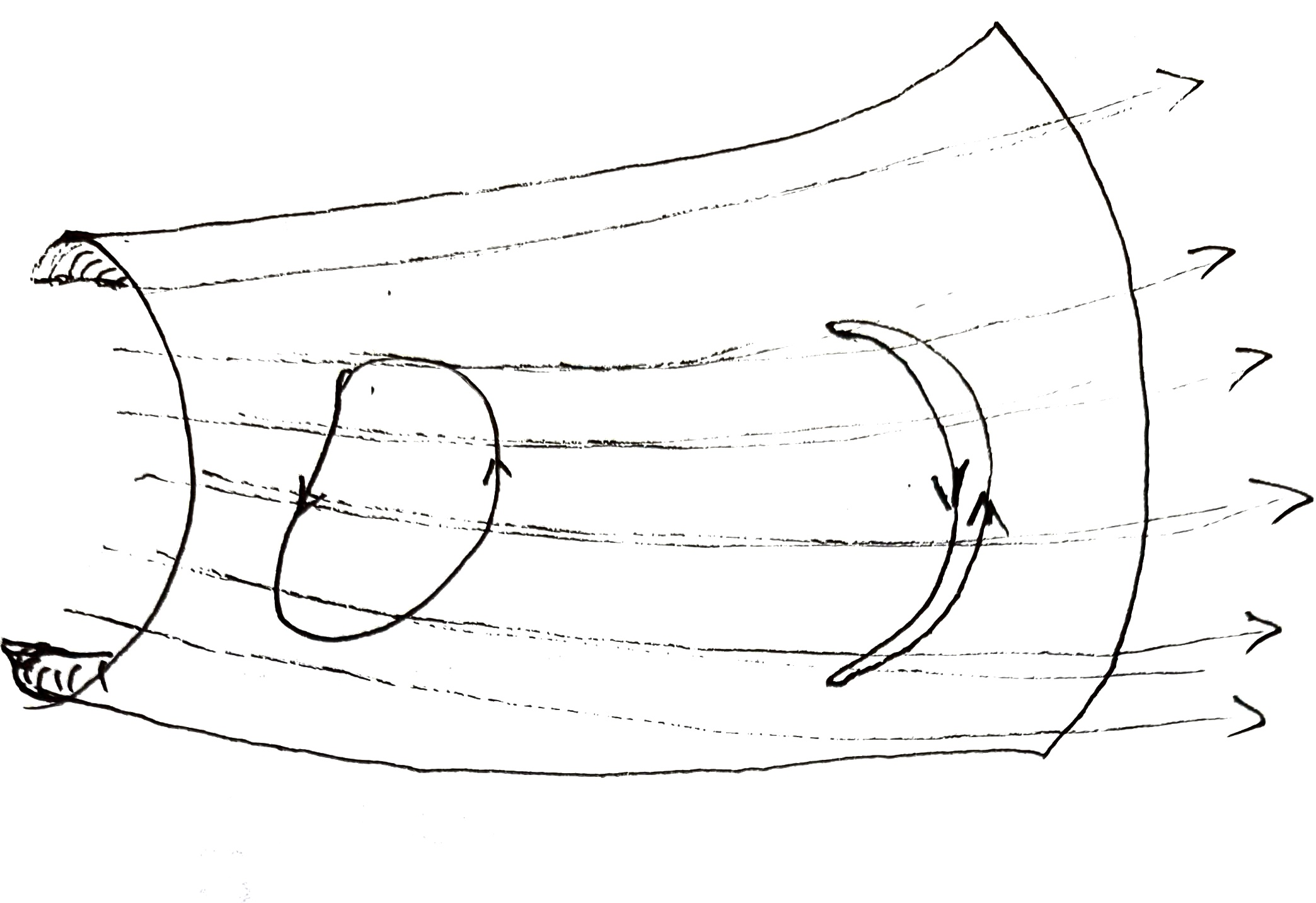

Exercise 3 A one-dimensional family of trajectories in phase space sweep out a curved surface. As shown in the illustration, prove that for any cycle \gamma on the curved surface, \oint_\gamma \left\langle p, dq\right\rangle = 0.

Two more proofs of HJE

We only need to prove p = \nabla S, which is sufficient to prove Equation 4, and thus the HJE. This we show by positional arbitrage.

Suppose that a physically real trajectory goes from (t_0, q_0) to (t, q). Now we consider a nearby trajectory: First, we go from (t_0, q_0) to (t, q + \delta q) by a physically real trajectory, then we sell off \delta q on the market. This would cost us

S(t, q+\delta q; t_0, q_0) - \left\langle p, \delta q\right\rangle = S(t, q; t_0, q_0) + \left\langle\nabla S - p, \delta q\right\rangle

If \nabla S \neq p, then we can take \delta q = -(\nabla S - p)\epsilon, and thus magically make the journey cost less by a first-order infinitesimal. This means the market is inefficient, a contradiction.

Here is a proof in the spirit of wave mechanics and dynamical programming. Though I did not study his proof,11 I believe this is how the inventor of dynamical programming, Richard Bellman, proved his extension, the Hamilton–Jacobi–Bellman equation. The HJBE reduces to the HJE under certain conditions – they do not talk about the same thing, because while HJ is about stationary action, HJB is about maximal action.

11 In his autobiography, he said,

Problems of this type had been worked on before by many mathematicians, Euler, Hamilton, and Steiner, but the systematic study of problems of this type was done at RAND starting in 1948 under the inspiration of von Neumann. (Bellman 1984, 208)

… one can use dynamic programming for the minimum principles of mathematical physics. For example, with dynamic programming one has a very simple derivation of the eikonal equation. In addition, the Hamilton–Jacobi equation of mechanics can easily be derived. (Bellman 1984, 289)

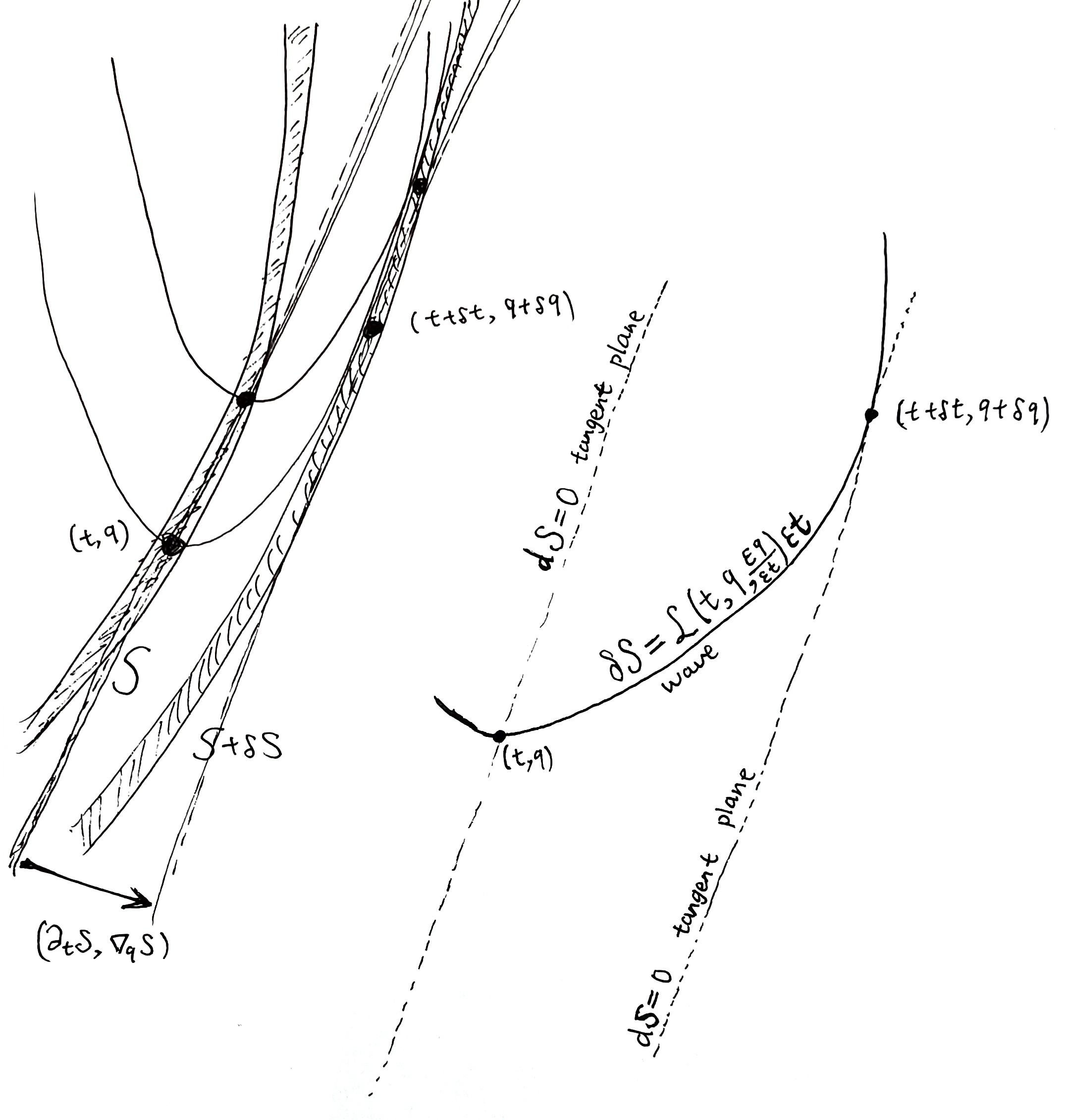

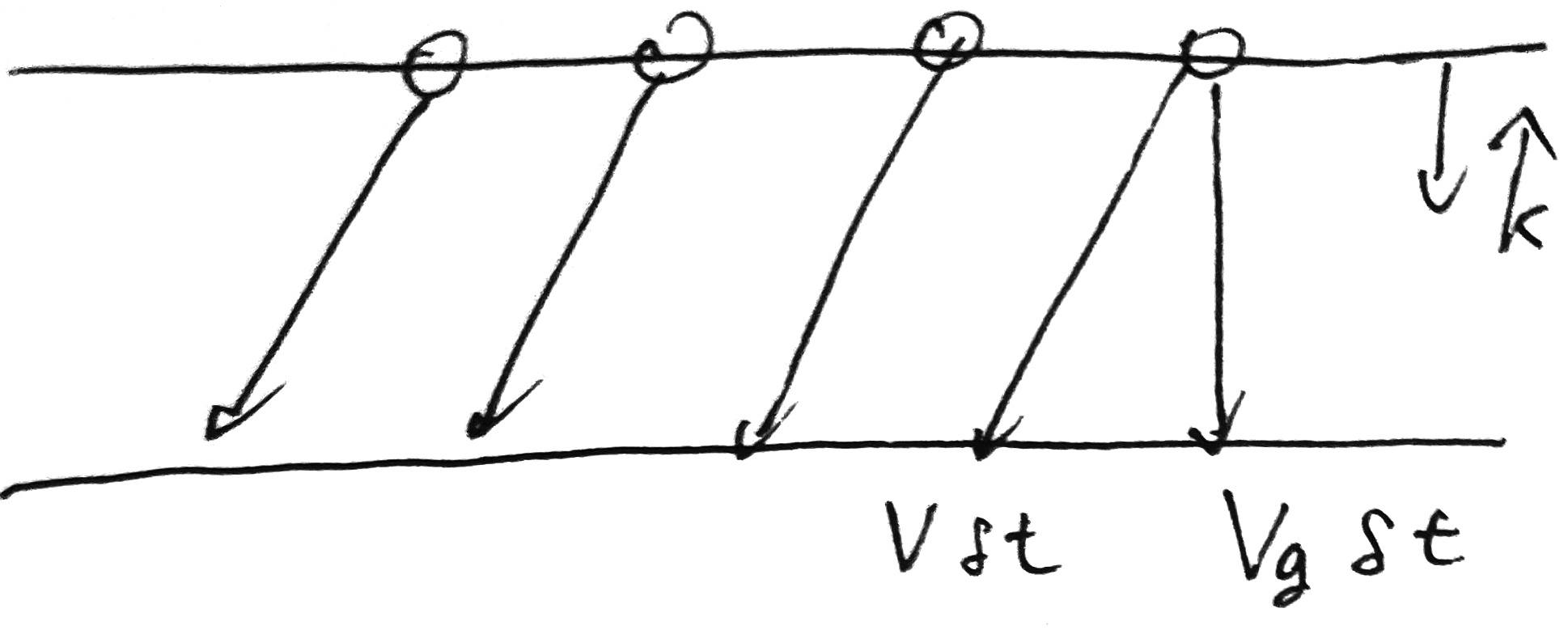

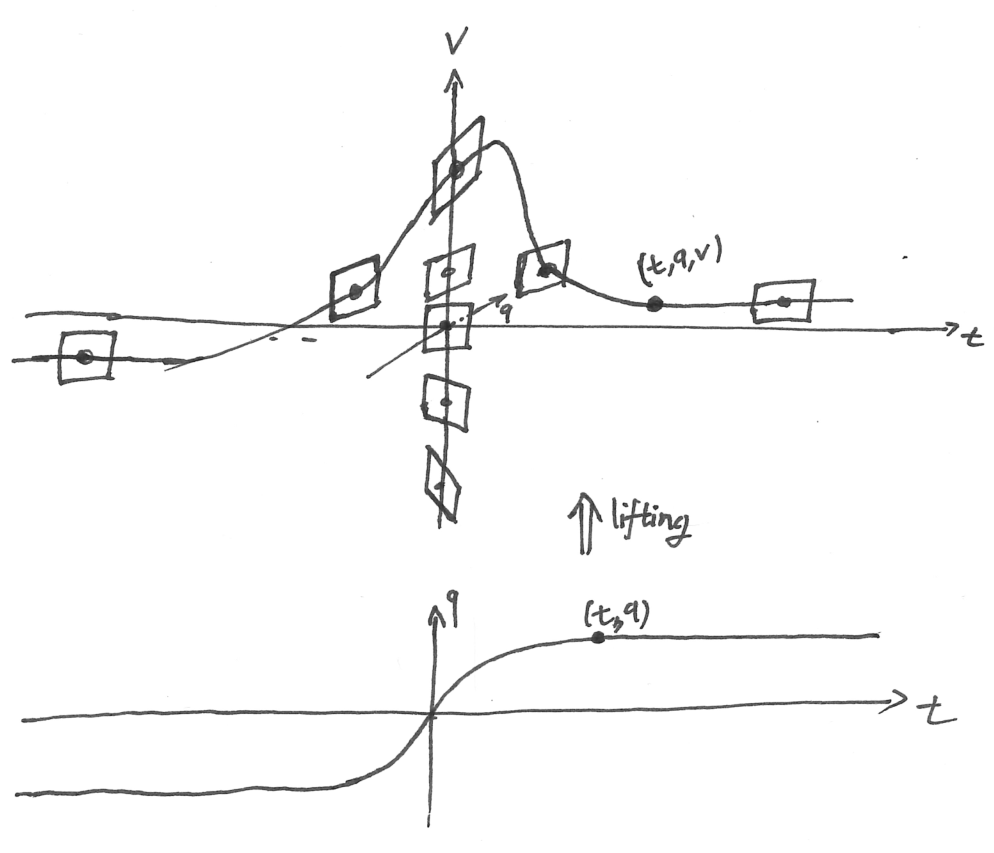

Suppose that we have found all points at which the action is equal to S. Now we would like to expand that surface a little further, to the surface of action S + \delta S. We do that in the spirit of economics (of course!) and traveling.

Interpret the action of a path as the cost of traveling along that path. The surfaces of constant action, then, become the isochrone maps. The problem we face is then a matter of travel planning: Given that we can reach up to surface X_S if we are willing to pay cost S, how much further can we travel if we are willing to pay an additional \delta S?

Let us stand at a point (t, q) on the surface of action S, and consider all the points we can reach by an additional action \delta S. Suppose we go from (t, q) to (t + \epsilon t, q + \epsilon q), then the cost of that is L\left(t, q, \frac{\epsilon q}{\epsilon q}\right)\epsilon t. (We write \epsilon t instead of \delta t, because we have to use that symbol later.)

Therefore, the “little waves” (“wavelets”) of action \delta S radiating out of the point (t, q) are those points (t + \epsilon t, q + \epsilon q) satisfying the equation

L\left(t, q, \frac{\epsilon q}{\epsilon t}\right)\epsilon t = \delta S

And the surface of action S + \delta S is the envelope of all those wavelets. This is the wave perspective, but we still need to return to the particle perspective.

Suppose you are already at (t, q), and you just want to reach the surface of S + \delta S. It doesn’t matter where you end up on that surface – you just have to get to that surface somewhere. You also have exactly \delta S to spend, so you have to plan optimally. So, you draw out the surface of all points you can reach after spending another \delta S. This is the \delta S-wavelet out of (t, q). Now, looking at that picture, you see that the only place you can possibly reach is a certain point (t + \delta t, q + \delta q).

Because the wavelet cannot reach beyond S + \delta S, it’s clear that the wavelet is tangent to the surface of S+\delta S precisely at (t + \delta t, q + \delta q). But we can go further. We claim that the tangent surface of S at (t, q) is exactly parallel to the tangent surface of S+\delta S at (t + \delta t, q + \delta q).

To see it, imagine nudging (t, q) around the surface of S. As you nudge around, the wavelet also slides around. If the tangent surfaces are not exactly parallel, then you can find a good direction to nudge the point (t, q), such that as you give it a good shove, the wavelet bursts through the surface of S + \delta S, creating a contradiction.

That is, we have shown that there are 3 tangent planes, all parallel to each other:

- The tangent plane of S at (t, q).

- The tangent plane of S + \delta S at (t + \delta t, q + \delta q).

- The tangent plane at (t + \delta t, q + \delta q), of the \delta S-wavelet radiating out of (t, q).

We write out symbolically the fact that Plane 1 is parallel to Plane 3:

\begin{aligned} & \quad \underbrace{dS}_{\text{Plane 1}} \\ &= \partial_t S + \left\langle\nabla_q S, dq\right\rangle \\ &\propto \underbrace{d\Bigg|_{\epsilon t = \delta t, \epsilon q = \delta q}\left(L\left(t, q,\frac{\epsilon q}{\epsilon t}\right) \epsilon t\right)}_{\text{Plane 3}} \\ &= \left(L-\frac{\delta q}{\delta t} \nabla_v L\right) dt + \left\langle\nabla_v L, dq\right\rangle\\ \end{aligned}

Thus, there exists some constant c > 0 such that

(\partial_t S, \nabla_q S) = c \left(L - \left\langle\nabla_v L, \frac{\delta q}{\delta t}\right\rangle , \nabla_v L\right) = (-cH, cp)

This is the HJE, once we prove that c=1. To prove it, note that, by construction, the straight path from (t, q) to (t + \delta t, q + \delta q) is an optimal way to reach S + \delta S from S, therefore it costs exactly \delta S, so

\delta S = L \delta t

which means

\partial_t S \delta t + \left\langle\nabla_q S, \delta q\right\rangle = L\delta t = \left(L - \left\langle\nabla_v L, \frac{\delta q}{\delta t}\right\rangle\right)\delta t + \left\langle\nabla_v L, \delta q\right\rangle

Thus, c=1.

If the wavelet is convex, then the tangent point is unique, and there is only one way to proceed from (t, q). However, if the wavelet is not, then there could exist two or more particle paths shooting out from (t, q). It is similar to birefringence and conical refraction (Lunney and Weaire 2006).

Exercise 4 If you have studied, or intend to study, control theory, then prove the Hamilton–Jacobi–Bellman equation using the exact same picture. You can also prove the stochastic HJB equation in the same way, though you would need to insert the expectation \mathbb{E} somewhere.

Hamilton characteristic function

In many situations, the dynamics of the system is time-independent. That is, H does not depend on time. This simplifies the HJE to

\partial_t S = -H(q, \nabla_q S)